Ahead of the release of the Brokers on Banks surveys results this week, take a look at what you said about banks’ products and channel conflict

The full Brokers on Banks 2020 report will come out this Wednesday in MPA Magazine. In the meantime, here’s a preview of some of the things we’ll be covering.

Eighteen months ago, interest rates were increasing as global funding costs put greater pressure on the banks. In fact, just a year ago, we were talking about increasing rates in this report. But soon after, these pressures decreased, and the RBA began cutting rates, which allowed the banks to cut their own.

Eighteen months ago, interest rates were increasing as global funding costs put greater pressure on the banks. In fact, just a year ago, we were talking about increasing rates in this report. But soon after, these pressures decreased, and the RBA began cutting rates, which allowed the banks to cut their own.

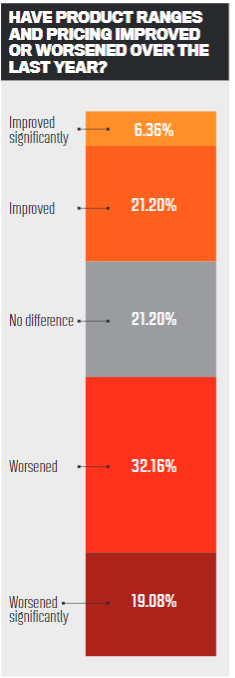

Now, rates in Australia are at record lows. This possibly explains why more than 54% of brokers responding to our survey said product ranges and pricing had improved – although the response was similar last year.

In the survey, we asked brokers whether they thought banks were passing on the best savings to customers, considering the low interest rates. Respondents listed banks like Bankwest, Macquarie and ING, which were the top three in the interest rate category. Other banks listed included AMP, St. George and regional bank Heritage.

“The non-majors have passed on greater savings, have better upfront rates without the need to ask for pricing, such as Macquarie Bank,” said one broker.

While many said some were passing on savings, others were not so convinced.

“None of the banks are passing on the savings to existing customers. The gap between what banks are offering to new clients and what their existing clients are receiving is astonishing. Sometimes it can be as much as 1%. For new clients the second-tier lenders are passing on bigger savings,” said a broker.

Business going to certain banks

Interest rates and product ranges are an important factor when brokers choose to use certain banks. In the survey, we asked if brokers had given more business to a particular bank in the past 12 months, and why.

Most brokers pointed to product ranges and policy as their main reasons for sending loans to banks. One broker said they had sent more business to certain banks because of their products, rates and policies – backed by good, consistent turnaround times.

“I have majority of IO investment loans going to Virgin Money due to their competitive rates, velocity points and low fees, as well as servicing,” said another.

One broker said they used Macquarie because of its rates and service and ANZ for its product offering and the number of different options it could provide.

Channel conflict still an issue

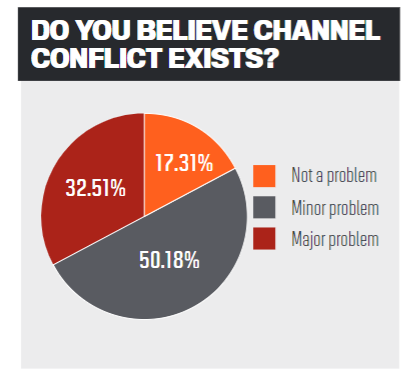

Channel conflict has also been highlighted as a continuing problem. More than 80% of respondents said it was a minor or major issue, although this was slightly lower proportion than in the previous two years. Asked at which banks they’d had a particular experience with channel conflict, the top three picked by brokers were all major banks.

One broker said, “They all have best interest duty to themselves. Channel conflict is alive and well.”

Several brokers also talked about banks phoning their clients and trying to entice them away, but one said it was not necessarily the banks’ fault.

“I find that it is individuals at organisations that cause the conflict,” they said. “The lender can see in the system that the loan has been introduced to the bank via a broker, and yet they still internally refinance the loan, offering lower rates and cashback, which is not available via the broker channel.

“I have had instances where the bank staff advise the client they should not have engaged a broker at all, and that we are only doing business to be paid a commission and not acting in the best interest of the client.”