Brokers need to prepare themselves for further pricing and serviceability changes as regulators redouble their efforts to make Australia’s banks ‘unquestionably strong’

Regulator's aren't renowned for straight talking. So when regulators do sound the alarm bells, the industry tends to respond.

Speaking at the Australian Financial Review’s recent Banking and Wealth Summit, the Basel Committee’s secretary general Bill Coen made a chilling prediction. “I’m an optimist by nature but maybe a pessimist by fact and experience. We know with statistical certainty there will be another financial crisis.”

Coen is not an Australian regulator, nor the head of an Australian bank. The Basel Committee is perhaps the closest we have to a global regulator. Based in Switzerland, they set the standards by which banks should abide, the most well known of which being how much capital a bank must hold. When APRA increased capital requirements in 2015 – causing interest rate rises for many customers – they attributed it in part to the “direction of work being undertaken by the Basel Committee”.

Therefore, when Basel talks APRA listens, as APRA chairman Wayne Byres made clear later that day at the summit. “When adversity arrives – it is not ‘if’, it will – to the extent possible we want the banking system to help alleviate rather than exacerbate problems.” With adversity a certainty, regulators needed to prepare for trouble now, he argued. “It is better we continue to invest in building resilience now when it can be done in an orderly manner from a position of relative strength than try to do so in more difficult times.”

More than seven years on from the GFC, it can be surprising, if not alarming, to hear regulators talk in such terms, especially given Australia’s banks fared relatively well. Evidently regulators are serious, which means lenders and brokers need to see further changes as a serious possibility, not just now, but for several years to come.

come.

Unquestionably strong

Many interpreted 2015 as the year of upheaval, with APRA raising capital requirements for the major banks, as well as attempting to limit finance to property investors. In October, the government agreed to the proposals of the Financial System Inquiry (otherwise known as the Murray Inquiry), which proposed “setting Australian bank capital ratios such that they are unquestionably strong by being in the top quartile of internationally active banks.”

What was made clear at the AFR’s summit is that capital requirements continue to be an issue, and aren’t going away any time soon. APRA chairman Byres told delegates that “our consideration of what constitutes ‘unquestionably strong’ in an Australian context will need to wait until around the end of the year. The direction is pretty clear – no one should be planning for capital requirements to decline”.

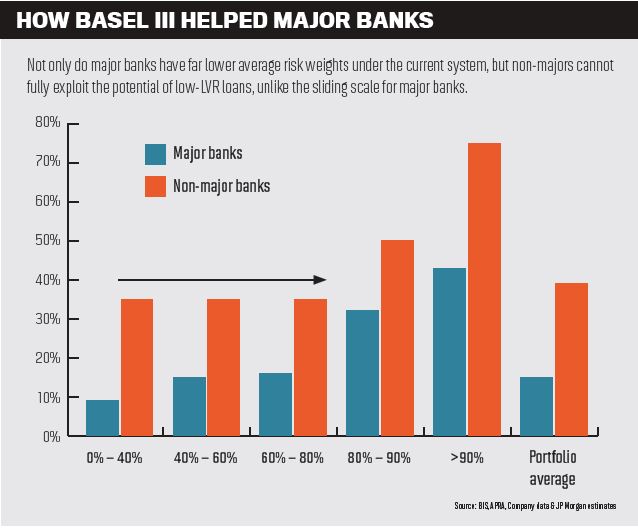

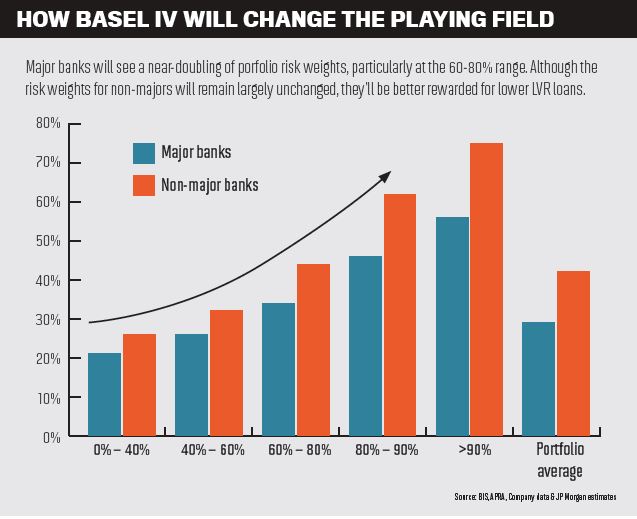

In a similar vein, Coen explained that the Basel committee was looking to encourage banks to calculate the amount of capital they need in a different way, as well as encouraging use of the standardised model. “The committee is promoting greater restrictions on the use of IRB models,” he said. Internal risk-based models (IRB) is the system used by Australia’s major banks and Macquarie. If the banks were to move towards the standardised model, used by the non-majors, they would need to find significantly more capital, which could require further rate rises.

Regulating beyond capital

Capital was, however, just one of four areas of focus for APRA in the current year, noted Byres. The others were: Improving the stability of liquidity and funding profiles; enhancing both the public and private sectors’ readiness for adversity; and strengthening the risk culture within the financial system. Of these, it is risk culture that has had the most interest, because it is being applied to the broker channel itself.

Culture is usually identified more closely with another regulator – ASIC, but has become a mantra for the entire financial industry. “No regulatory speech these days is complete without a few words on the issue of culture,” Byres joked. “We need the financial sector to take up the challenge to put in place better incentives for prudent behaviour, so as to prevent problems emerging in the first place. That is likely to be far more productive than spending our time removing so-called ‘bad apples’ after the fact.”

Whilst ASIC’s ongoing broker remuneration review was ordered by the government, it has certainly been framed by the language of culture; whether commission is encouraging brokers to do the wrong thing by the customer. More widely, both regulators want company directors to encourage a good culture in their organisations. As ASIC chairman Greg Medcraft told delegates later in the AFR’s summit: “At the end of the day, companies need to have a culture that customers can believe in. And recent events put that into question.”

Whilst ASIC’s ongoing broker remuneration review was ordered by the government, it has certainly been framed by the language of culture; whether commission is encouraging brokers to do the wrong thing by the customer. More widely, both regulators want company directors to encourage a good culture in their organisations. As ASIC chairman Greg Medcraft told delegates later in the AFR’s summit: “At the end of the day, companies need to have a culture that customers can believe in. And recent events put that into question.”

Lenders’ reactions

Making speeches is very different to making policy, of course, and what makes the difference is the degree of opposition to regulators’ proposals. However, the dissenting voices at AFR’s summit were few and far between, even from the banks. NAB chairman Ken Henry, delivering his keynote on ‘the future of banking’, said that the regulator’s interest in culture was “understandable” and that “culture drives conduct”.

Henry suggested the banks that would succeed over the next decade would be those with a strong customer-focused culture, which included working with the regulators. Indeed, Henry added that just paying more attention to compliance was not the same as a good culture, “just as slowing down whilst passing stationary speed cameras is not the same thing as safe driving.”

In our recent Banks on Brokers report, the third party heads of Westpac, CBA, ANZ, Suncorp and Macquarie positively reacted to recent regulatory changes. Tony MacRae, general manager third party distribution at Westpac and St George Group, said the bank was “happy to see the attention that the regulators are putting on the home loan origination process”, because it helped the bank become more sustainable and robust. Similarly, Macquarie commented: “We support APRA’s approach to ensuring there is sustainable and prudent lending.”

The only note of reluctance – and a limited one at that – came from CBA’s general manager of broker sales Sam Boer, who argued that the bank was already maintaining an “unquestionably strong capital position”. Further regulation needed to be carefully thought through, he added. “Any changes required to make the Australian banking system more secure needs to be balanced with the interests of our customers, as well as the nearly 800,000 households who are direct shareholders of Commonwealth Bank and the millions more who are invested through their superannuation funds.”

The only note of reluctance – and a limited one at that – came from CBA’s general manager of broker sales Sam Boer, who argued that the bank was already maintaining an “unquestionably strong capital position”. Further regulation needed to be carefully thought through, he added. “Any changes required to make the Australian banking system more secure needs to be balanced with the interests of our customers, as well as the nearly 800,000 households who are direct shareholders of Commonwealth Bank and the millions more who are invested through their superannuation funds.”

What can lenders and brokers do?

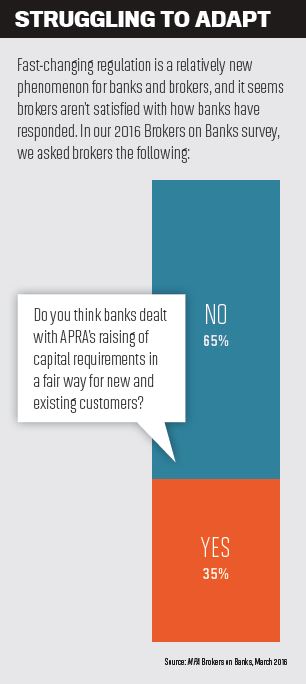

Evidently, 2015 was not an exceptional year. More regulation is on the horizon and brokers and lenders will need to get used to an environment of uncertainty. Yet the experience of 2015 suggests the third party channel struggles to deal with APRA’s changes in an organised way. In our recent Brokers on Banks survey, we asked brokers whether the banks had dealt with changing capital requirements in a fair way for new and existing customers – and 65% of respondents said they hadn’t.

Whilst many respondents understood that APRA’s changes to capital requirements were behind the rate rises, they took issue with the way banks initiated and communicated rate rises. We asked MacRae from Westpac – the first bank to raise rates – whether they’d communicate future changes in a different way. “Last year was a year with a particularly high volume of changes,” explained MacRae. “We were all moving quickly and reacting, and in those environments we can all learn. In terms of communicating the ‘why’ and positioning in a more robust way is an opportunity for all of us.”

One interesting example of ‘communicating the why’ was given by Doug Lee, head of mortgage sales at Macquarie Bank. The bank started by organising meetings with key brokers’ partners “to provide a regulatory background update and took them through the changes and what the potential impact of those changes may be”. They followed this up with a national road show “dedicated to explain and educate brokers on the regulatory landscape and the changes and potential impacts, including policy and pricing”.

Macquarie are proud of being on the ‘front foot’ in responding to APRA’s changes. This hasn’t always been popular with brokers however. When NAB Broker sent letters to customers informing them of the changes, many brokers saw this as going behind their back, as they told our Brokers on Banks survey in their comments. With brokers looking to establish long-term customer relationships based on expertise, having anxious customers wondering why their broker didn’t tell them about the rate rise is a situation they’d rather avoid.

If brokers want to continue to be the main focus of expertise and information for their customer, they’ll need to put themselves on the front foot ahead of the banks. Last year, several aggregators and franchises produced on this extra role can be seen as a major opportunity, as ANZ’s head of third party Keiran Evans explains. “Change is always difficult, however we believe it provides opportunities for brokers to demonstrate their knowledge and expertise and help guide customers to the best outcome.”

Speaking at the Australian Financial Review’s recent Banking and Wealth Summit, the Basel Committee’s secretary general Bill Coen made a chilling prediction. “I’m an optimist by nature but maybe a pessimist by fact and experience. We know with statistical certainty there will be another financial crisis.”

Coen is not an Australian regulator, nor the head of an Australian bank. The Basel Committee is perhaps the closest we have to a global regulator. Based in Switzerland, they set the standards by which banks should abide, the most well known of which being how much capital a bank must hold. When APRA increased capital requirements in 2015 – causing interest rate rises for many customers – they attributed it in part to the “direction of work being undertaken by the Basel Committee”.

Therefore, when Basel talks APRA listens, as APRA chairman Wayne Byres made clear later that day at the summit. “When adversity arrives – it is not ‘if’, it will – to the extent possible we want the banking system to help alleviate rather than exacerbate problems.” With adversity a certainty, regulators needed to prepare for trouble now, he argued. “It is better we continue to invest in building resilience now when it can be done in an orderly manner from a position of relative strength than try to do so in more difficult times.”

More than seven years on from the GFC, it can be surprising, if not alarming, to hear regulators talk in such terms, especially given Australia’s banks fared relatively well. Evidently regulators are serious, which means lenders and brokers need to see further changes as a serious possibility, not just now, but for several years to

come.Unquestionably strong

Many interpreted 2015 as the year of upheaval, with APRA raising capital requirements for the major banks, as well as attempting to limit finance to property investors. In October, the government agreed to the proposals of the Financial System Inquiry (otherwise known as the Murray Inquiry), which proposed “setting Australian bank capital ratios such that they are unquestionably strong by being in the top quartile of internationally active banks.”

What was made clear at the AFR’s summit is that capital requirements continue to be an issue, and aren’t going away any time soon. APRA chairman Byres told delegates that “our consideration of what constitutes ‘unquestionably strong’ in an Australian context will need to wait until around the end of the year. The direction is pretty clear – no one should be planning for capital requirements to decline”.

In a similar vein, Coen explained that the Basel committee was looking to encourage banks to calculate the amount of capital they need in a different way, as well as encouraging use of the standardised model. “The committee is promoting greater restrictions on the use of IRB models,” he said. Internal risk-based models (IRB) is the system used by Australia’s major banks and Macquarie. If the banks were to move towards the standardised model, used by the non-majors, they would need to find significantly more capital, which could require further rate rises.

Regulating beyond capital

Capital was, however, just one of four areas of focus for APRA in the current year, noted Byres. The others were: Improving the stability of liquidity and funding profiles; enhancing both the public and private sectors’ readiness for adversity; and strengthening the risk culture within the financial system. Of these, it is risk culture that has had the most interest, because it is being applied to the broker channel itself.

Culture is usually identified more closely with another regulator – ASIC, but has become a mantra for the entire financial industry. “No regulatory speech these days is complete without a few words on the issue of culture,” Byres joked. “We need the financial sector to take up the challenge to put in place better incentives for prudent behaviour, so as to prevent problems emerging in the first place. That is likely to be far more productive than spending our time removing so-called ‘bad apples’ after the fact.”

Whilst ASIC’s ongoing broker remuneration review was ordered by the government, it has certainly been framed by the language of culture; whether commission is encouraging brokers to do the wrong thing by the customer. More widely, both regulators want company directors to encourage a good culture in their organisations. As ASIC chairman Greg Medcraft told delegates later in the AFR’s summit: “At the end of the day, companies need to have a culture that customers can believe in. And recent events put that into question.”Lenders’ reactions

Making speeches is very different to making policy, of course, and what makes the difference is the degree of opposition to regulators’ proposals. However, the dissenting voices at AFR’s summit were few and far between, even from the banks. NAB chairman Ken Henry, delivering his keynote on ‘the future of banking’, said that the regulator’s interest in culture was “understandable” and that “culture drives conduct”.

Henry suggested the banks that would succeed over the next decade would be those with a strong customer-focused culture, which included working with the regulators. Indeed, Henry added that just paying more attention to compliance was not the same as a good culture, “just as slowing down whilst passing stationary speed cameras is not the same thing as safe driving.”

In our recent Banks on Brokers report, the third party heads of Westpac, CBA, ANZ, Suncorp and Macquarie positively reacted to recent regulatory changes. Tony MacRae, general manager third party distribution at Westpac and St George Group, said the bank was “happy to see the attention that the regulators are putting on the home loan origination process”, because it helped the bank become more sustainable and robust. Similarly, Macquarie commented: “We support APRA’s approach to ensuring there is sustainable and prudent lending.”

The only note of reluctance – and a limited one at that – came from CBA’s general manager of broker sales Sam Boer, who argued that the bank was already maintaining an “unquestionably strong capital position”. Further regulation needed to be carefully thought through, he added. “Any changes required to make the Australian banking system more secure needs to be balanced with the interests of our customers, as well as the nearly 800,000 households who are direct shareholders of Commonwealth Bank and the millions more who are invested through their superannuation funds.”What can lenders and brokers do?

Evidently, 2015 was not an exceptional year. More regulation is on the horizon and brokers and lenders will need to get used to an environment of uncertainty. Yet the experience of 2015 suggests the third party channel struggles to deal with APRA’s changes in an organised way. In our recent Brokers on Banks survey, we asked brokers whether the banks had dealt with changing capital requirements in a fair way for new and existing customers – and 65% of respondents said they hadn’t.

Whilst many respondents understood that APRA’s changes to capital requirements were behind the rate rises, they took issue with the way banks initiated and communicated rate rises. We asked MacRae from Westpac – the first bank to raise rates – whether they’d communicate future changes in a different way. “Last year was a year with a particularly high volume of changes,” explained MacRae. “We were all moving quickly and reacting, and in those environments we can all learn. In terms of communicating the ‘why’ and positioning in a more robust way is an opportunity for all of us.”

One interesting example of ‘communicating the why’ was given by Doug Lee, head of mortgage sales at Macquarie Bank. The bank started by organising meetings with key brokers’ partners “to provide a regulatory background update and took them through the changes and what the potential impact of those changes may be”. They followed this up with a national road show “dedicated to explain and educate brokers on the regulatory landscape and the changes and potential impacts, including policy and pricing”.

Macquarie are proud of being on the ‘front foot’ in responding to APRA’s changes. This hasn’t always been popular with brokers however. When NAB Broker sent letters to customers informing them of the changes, many brokers saw this as going behind their back, as they told our Brokers on Banks survey in their comments. With brokers looking to establish long-term customer relationships based on expertise, having anxious customers wondering why their broker didn’t tell them about the rate rise is a situation they’d rather avoid.

If brokers want to continue to be the main focus of expertise and information for their customer, they’ll need to put themselves on the front foot ahead of the banks. Last year, several aggregators and franchises produced on this extra role can be seen as a major opportunity, as ANZ’s head of third party Keiran Evans explains. “Change is always difficult, however we believe it provides opportunities for brokers to demonstrate their knowledge and expertise and help guide customers to the best outcome.”