With both the property and business markets struggling, unsecured business loans are providing a way out for many

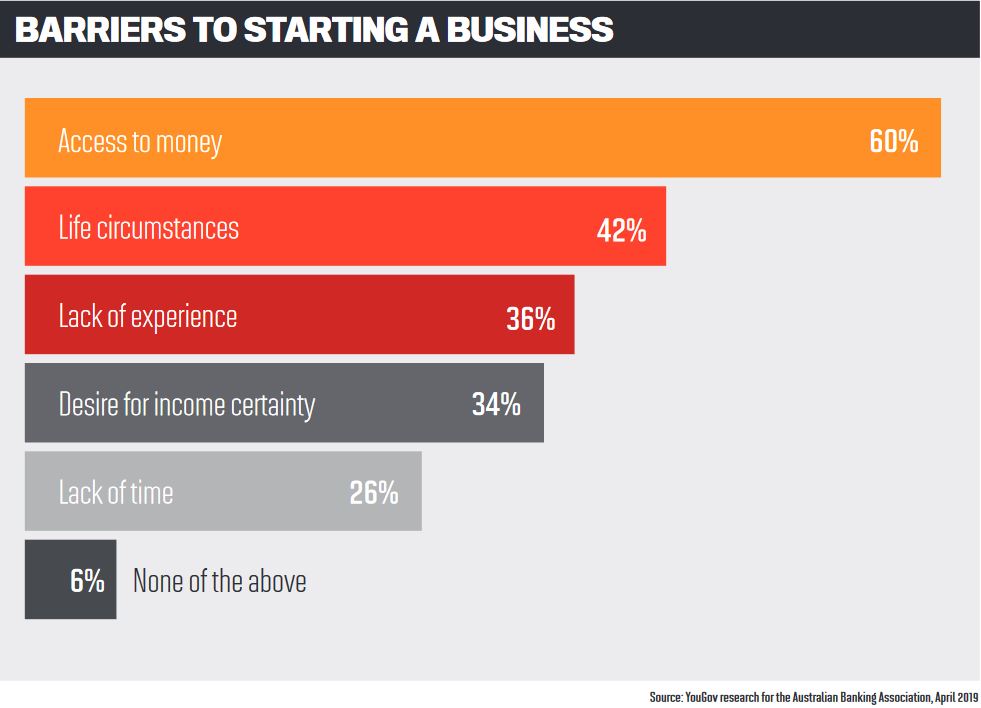

When asked what was holding them back from starting a new business, 60% of Australians said it was access to finance, according to YouGov research last year on behalf of the Australian Banking Association.

While there are a number of options businesses can consider when it comes to finance solutions, new or potential business owners struggle to get the capital they need. Furthermore, in the September 2019 SME Growth Index published by Scottish Pacific, only 5.5% of SMEs wanted to use their property as security for loans.

“Most brokers out there are experienced and really understand the various finance products that are on offer” Yanir Yakutiel, Lumi

The option of unsecured business lending could be the solution they are after.

An unsecured business loan does exactly what its name says: it is a loan not secured by an asset. Instead, the lender will look at the business itself to determine its creditworthiness.

Whether businesses want to use an unsecured business loan to purchase an asset or piece of equipment, to pay invoices and boost their cash flow, or to pay their staff's salaries, this type of loan acts as a shortterm solution so they can get their businesses back on track.

Bill Baker, CEO of lend.com.au, says managing cash flow is the most difficult part of being a startup.

“Getting to the next stage you either have to borrow money from family, or you have to have some form of security in order to get the funds into your business,” he says. “Without either one of those it’s not very easy to grow your business and this is where the unsecured business loans come into their own.”

Understanding unsecured business loans

Understanding unsecured business loans

For a lender to determine whether it might want to offer an unsecured business loan to a borrower, it often looks at things like the projected cash flow of the business, the time in business, recent bank statements, and what the cyclical life of the business is.

“Just because the economy has come to a standstill, that doesn’t mean your bills have stopped; people have still got to live” Bill Baker, Lend.com.au

Lenders may typically also ask for a personal guarantee from the director of the business, leaving the guarantor personally responsible if the business cannot meet its obligations.

Yanir Yakutiel, founder and CEO of unsecured lender Lumi, says this typically applies to those businesses that don’t have any tangible assets to use as collateral, such as a cafe or restaurant that needs to buy stock or inventory.

This does not mean that a business owner cannot use an unsecured business loan for an asset purchase, however. For business owners, the number of finance solutions can be overwhelming, particularly if they overlap.

Yakutiel says this is where the experience and skill of a good broker comes into play. “Most brokers out there are experienced and really understand the various finance products that are on offer,” he says.

Brokers working with their business customers will need to understand what the business is trying to achieve, what the cash flow profile of the business is, and what the risk profile and price stability of the borrower look like.

Every business is different, Yakutiel explains. While some business owners may be happy to take out a second mortgage as security, others may want to pay a little bit more and take out an unsecured loan so they don’t put their home at risk.

He says Lumi sees scenarios in which borrowers have multiple businesses and want to use the equity in their house to support just one of those, or there may be multiple owners of the business and they like to segregate because no one wants to put their house on the line.

“Like anything else, it becomes about risk allocation and pricing for that risk and finding the most suitable product to meet those specifications of the customer,” he says.

“That’s why we think brokers are really important, and brokers play a really important part in our distribution strategy, because they are there with the customer. They understand the customer a lot better than us.”

The impact of COVID-19

The problem of offering unsecured business lending in the current environment is that lenders will find it hard to ascertain the creditworthiness of a business in such difficult circumstances. Yakutiel says that while current demand for unsecured business loans is “through the roof ”, the suitability of this type of lending has gone down because businesses are having such massive impacts on their cash flow.

“The problem is that it’s very hard to underwrite deals based on traditional models [at the moment],” he explains.

“The traditional models are based on the business trading, having a consistent cash flow, etc., and that’s already been thrown into the wind because of the coronavirus.”

For the short term, Yakutiel says, either secured products or longer-term unsecured products will be more relevant, but he remains positive.

“I think once things start levelling out in the next three, four months and businesses start trading out, the demand for unsecured lending is going to keep growing at an exponential rate,” he says.

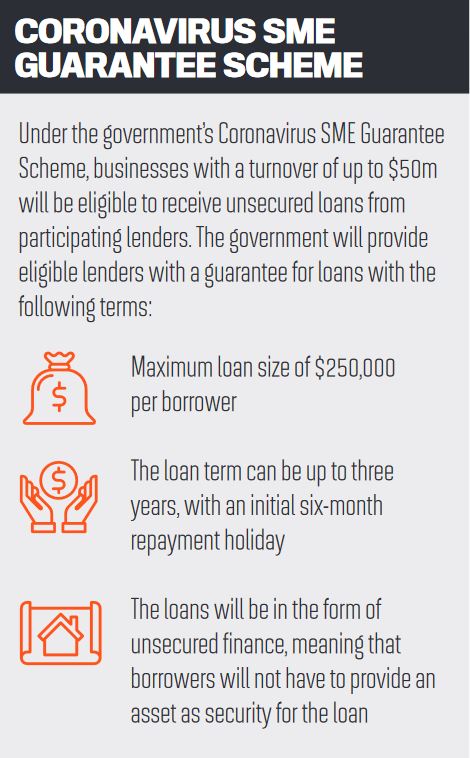

One positive for unsecured business lending right now is the government’s Coronavirus SME Guarantee Scheme that will see them provide a guarantee of 50% to SME lenders for new unsecured loans to be used by eligible businesses as working capital.

The aim of the scheme was to ensure the lenders’ willingness and ability to provide credit to SMEs so they could survive the coming months.

“Brokers play a really important part in our distribution strategy, because they are there with the customer. They understand the customer a lot better than us” Yanir Yakutiel, Lumi

But according to research by Lend.com.au back in April, four in five businesses did not believe banks could approve and settle these loans as fast as they needed it. One in three businesses believed that non-banks would be able to deliver these loans faster.

In the same survey, 70% of respondents said they needed the finance to survive, and 12% said the timing was already too late for their business.

Lend.com.au’s Baker says the timing was so important for these businesses because many of them did not know if they could keep their staff or pay their bills.

“Just because the economy has come to a standstill, that doesn’t mean your bills have stopped; people have still got to live,” he says. “We all need money to survive, and this is why having this speed of access to funds is the most crucial part. Building a business takes a long time – finding the right staff, making sure you’ve got the right supply chain; you need to make sure you’ve got the right structure, and all that takes a long time for a small business to build.

“To wipe that overnight because you can’t afford to keep your staff, or you can’t afford to keep your current suppliers, when that disappears really quickly, for someone to start rebuilding again, most people won’t be able to do that.”

However, Baker adds that brokers are in a good position because they understand their clients’ needs.

“At the moment there’s a lot of confusion coming from the lenders, and this is where the problem lies,” he says.

“Unfortunately, the problem is there’s going to be a bottleneck, because everyone’s going to process applications all at once. Once the lender comes out and says ‘these are my rules of lending to an SME’, then the broker will be able to capitalise on that really quickly.”