Lenders are looking to support SMEs seeking funding for growth, and this means more opportunities for brokers

For small business owners, getting access to finance has always been a struggle. During COVID-19 this became much harder, but it looks like things are turning around.

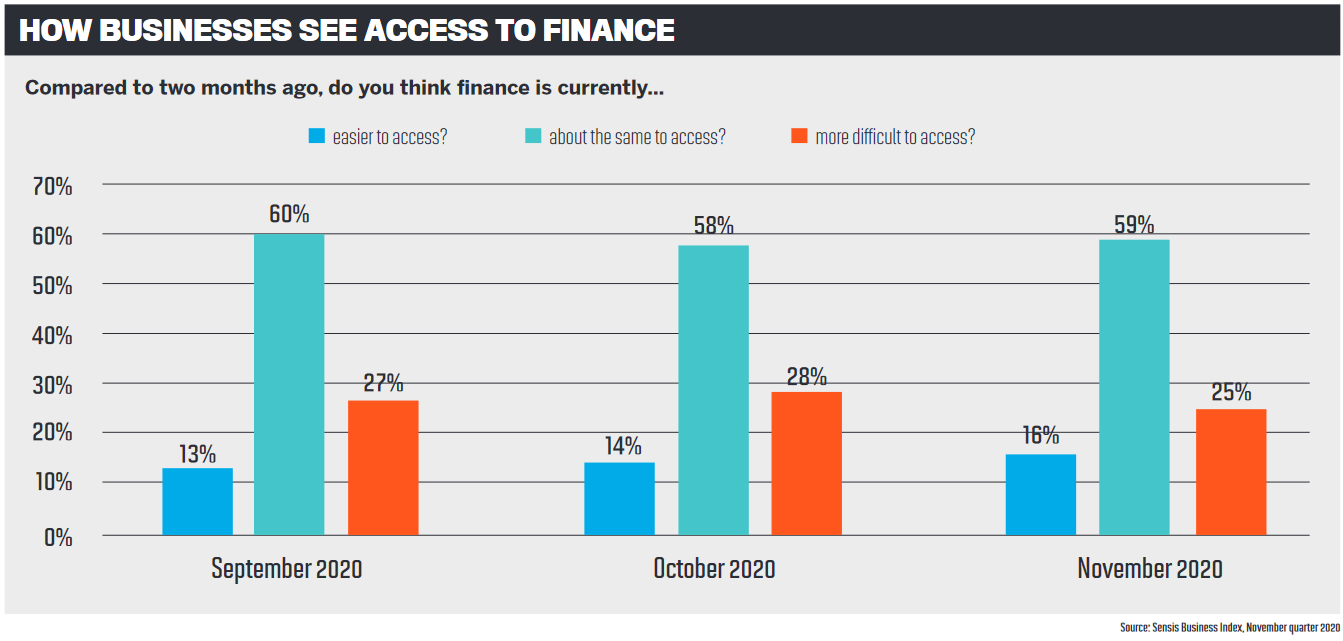

In the quarter to March 2020 – before the pandemic really struck – 32% of SMEs said it was more difficult to access finance than in the quarter before, according to the Sensis Business Index. By the time August 2020 came around, this figure had risen to 37%.

Taking a closer look at the month-by-month change in the following quarter, it’s clear that businesses became more and more confident in 2020 about their ability to access finance with each passing month. By November, only 25% of SMEs said it was harder to access finance.

However, the drop did not equate to a change in how easy businesses were finding access to finance – instead, more SME owners were saying it was just as difficult as it was two or three months before.

From its brokers’ point of view, AFG says lenders showed “a fair bit of caution” throughout the difficult lending period brought on by COVID-19, and they were offering a range of different products for different scenarios. Because of this, the aggregator focused on providing education and support, because small brokers “massively needed the help”.

“They’re so time-poor at the moment,” says David Drinkwater, AFG national sales manager, commercial and asset finance.

“They actually need some guidance and advice, and sometimes you can get that directly from the bank that you’re dealing with, but quite often dealing with one bank will give you a limited amount of products that you can use, and you may be chasing something different. So that’s where getting an educated broker who can get the customer’s best options is key, especially in a tough environment like we’ve just gone through.”

Agreeing on the importance of education during a difficult business period, AFG’s head of sales and distribution, Chris Slater, adds, “We just tried to provide as much support as we could for the customers themselves, but tried to empower our mortgage brokers to be as educated as they could about what was available for our customers.

“We had SME customers who took their home loan through AFG, for example, and they were in distress.”

At NAB, the bank is lending around $2.5bn every month to businesses. Chris Thomas, NAB executive, commercial broker and equipment finance sales, says 2020 was the biggest year it ever had through the broker channel, and 2021 is so far exceeding expectations.

The SMEs turning to NAB “come in all shapes and sizes”, but those needing finance might be sole proprietors looking for a small loan, farmers wanting to acquire new equipment for the harvest, or a large enterprise seeking expansion finance on a grand scale.

Currently, the dynamic of today’s SME market is “one of urgency”, Thomas says.

“The economy is evolving quickly, and SMEs are increasingly pivoting towards growth opportunities, requiring investment in all sectors.

“Interestingly we are seeing an uptick in SME mergers/acquisitions. COVID also seems to have accelerated generational change, and these transactions are very private in nature. As such we are witnessing that several brokers are leading the deal, which speaks volumes to the value that they bring.”

SMEs looking to boost cash flow

On top of the need for funding to invest in growth opportunities, the primary reason businesses are turning to small business lender OnDeck is for help with cash flow. The fintech saw very early on when the lockdowns were first announced that businesses were experiencing a “cash flow squeeze”.

It offers short-term unsecured business loans of $10,000 to $250,000, which are often used by SMEs to buy trading stock, for marketing activities, or to hire more staff, do renovations and repairs, purchase new tools and equipment, etc.

Oliver Wade, OnDeck’s head of marketing and partnerships, says it is worth remembering that not every has business struggled during the pandemic, with many pivoting to new markets or revenue streams.

“Our own independent research confirmed that SMEs needed cash flow to navigate the pandemic, and this continues to be the case as we see the economy rebound,” he says.

“Small business owners are renowned for their determination and willingness to adapt, and we are seeing a renewed sense of optimism among the SME community. This, coupled with the ability to access fast, efficient finance, is helping SMEs chart a fresh course for the future.”

SME lender Moula also saw businesses come to it for help with cash flow. Head of sales Tas Tzimos says some may have had a gap between payables and receivables, while others needed help bridging between projects.

“We often encounter businesses who win a contract or get hired to fulfil a project that will increase revenue in the future, but they need capital to scale up and cover costs before they actually get paid for the work,” Tzimos explains. “We also see many businesses seeking funds to purchase inventory or equipment, to cover tax debt, pay for overheads.”

In the early stages of the pandemic, Moula offered payment deferral options to help businesses overcome the initial challenges, and it also participated in the first phase of the SME Guarantee Scheme that allowed businesses to defer repayments on principal and interest loans for six months.

“Before the pandemic, we consistently were hitting records for new lending at Moula,” Tzimos says.

“During COVID, we saw a decline for several months, but that situation started to improve dramatically later in the year as business confidence returned. We also noticed a change in the sectors that we were lending to. For example, our lending to businesses in financial and insurance services, professional, scientific and technical services, and wholesale trade increased.”

The federal government’s SME Guarantee Scheme has played a big part in the recovery of many businesses. It was established towards the end of March 2020 and provided support of up to $40bn in lending to SMEs by guaranteeing 50% of new loans issued by participating lenders.

Westpac took part in the first phase and is currently involved in the second phase and the third phase, the SME Recovery Loan Scheme. The bank has seen many businesses take it up while also making the most of record-low interest rates to invest in their future growth. Customers across a range of industries have turned to Westpac for finance to expand their businesses or invest in office equipment, machinery and business stock.

The national head of commercial intermediaries at Westpac Group, Janelle Pearce, says that while many small businesses are still doing it tough, particularly those impacted by international border closures, others are moving back into growth mode. “We’ve seen some really positive economic data out recently, showing business confidence is high, and we’re confident that optimism will trans-late to growth in the near term,” Pearce says.

The pandemic has also forced some businesses to not only grow but change. Pearce says she has been inspired by the entrepreneurial nature of small businesses and how they have adapted, giving one of Westpac’s customers as an example.

“Manly Spirits, a boutique distillery on Sydney’s Northern Beaches, saw an opportunity last year to leverage the business’s equipment and skills to manufacture hand sanitiser, which was in short supply amid an unprecedented surge in demand from health professionals, businesses and the general public,” she says.

“Small businesses like this are securing finance and moving fast on their feet to navigate through the challenging period.”

Significant opportunity to diversify

As businesses like this continue to grow and adapt, there are plenty of opportunities for mortgage brokers to look at how they can do the same and help small business customers.

As businesses like this continue to grow and adapt, there are plenty of opportunities for mortgage brokers to look at how they can do the same and help small business customers.

After the outbreak of COVID-19, AFG saw a drop in the number of mortgage brokers diversifying into commercial lending as they faced into a busy residential period, but the numbers are now starting to pick up.

Drinkwater says the opportunity to diversify is “significant”. Compared to the 60% of home loans introduced by brokers, they only bring in about 20% of SME loans.

“While some lenders continue to close branches, it still creates that better opportunity to have that face-to-face with the customer, especially when you’re potentially already dealing with them in doing their mortgage lending,” he says.

Slater adds that around 25% of the customers that brokers service are SMEs, and with fintechs and SME lenders joining the market, the barriers to entry to the commercial space have lifted. But he says “it is very much about confidence”.

“One of the things our residential brokers struggle with is a bit of confidence,” Slater says. “To have the confidence to do [commercial lending], we find they’ve needed personal support, which is why we have the scenario line and dedicated commercial BDMs to support them.”

Acknowledging the research that shows businesses have often found it difficult to access finance, NAB says it focuses on a relationship-led model and providing a nimble and innovative approach to accessing finance. This includes helping brokers under-stand any nuances and changes to business models, and workshopping through any deals to help brokers “think outside the box” and build solutions.

For brokers looking to diversify, Thomas says the opportunities are real and growing significantly. He adds that diversifying into SME lending takes investment and commitment, as well as an appreciation of the differences between applying for business finance and home finance.

“Much of this comes down to relationships held and having a much longer-term view of the customer,” he says.

“It’s not uncommon to provide lending to a business customer four to five times a year, whereas with a home lending customer it might be once every three years. These differences are important.

“Spending time understanding the customer’s needs, being able to walk in their shoes, and having empathy and under-standing around the key opportunities and challenges facing their business are really the ‘secret sauce’ for diversifying into SME lending,” Slater adds.

As a fintech, OnDeck is able to use data and modelling to make its process for applying for SME loans much more straight-forward for the customer than applying for a home loan. The lender does not ask for any upfront asset security; it just requires a director’s guarantee.

“Our products are tailored to SME needs, and for us, transparency is the key feature that builds trust,” Wade says.

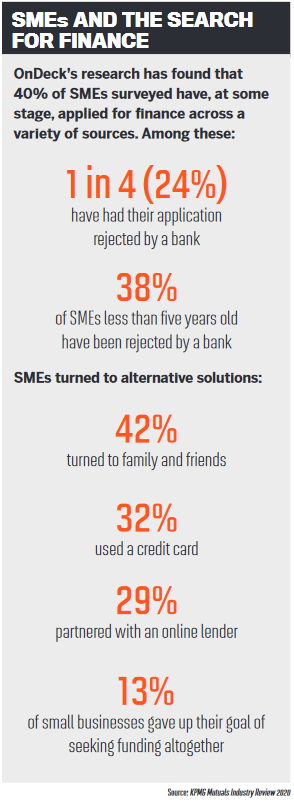

OnDeck’s own research has shown that one in four SMEs have been knocked back for bank finance, and among those that do get the green light, a further 25% say they experienced negative impacts because of the time it took to secure the finance.

As brokers can help their customers access easy finance from OnDeck, Wade says it provides a way to deepen their relationship with the client.

“Brokers need to see their business as a key investment – and, as with all investments, diversification is critical to supporting healthy long-term returns,” he says.

“By diversifying into commercial lending, brokers not only give their business exposure to a separate market, they can also enjoy faster loan turnaround times.”

SMEs seeking transparency and flexibility

Approving more loans each week, Moula is optimistic about economic growth and business confidence. Making it easier for mort-gage brokers to handle SME loans, the lender has just launched a referral process that gives brokers the choice of submitting a light-touch referral instead of a full application, and Moula will handle the rest.

“It’s been a great experience for brokers who don’t feel as confident about handling all the nuances of a business loan application,” says Tzimos.

Understanding that small businesses are frustrated with the difficulty of accessing finance, Moula takes this simple, no-nonsense approach to all of its loan applications. Tzimos explains that business owners want transparency, quick access to finance, the option of unsecured finance, the flexibility to repay their loans early, and short-term capital funding.

Mortgage brokers can offer this flexibility to Moula’s SME customers, and Tzimos says it is a simple way to diversify.

“More and more mortgage brokers are recognising the value of diversifying into SME lending,” he says.

“It creates an opportunity to contact their mortgage clients to offer additional products. It will also keep customers from going to other finance brokers who offer business lending and could eventually take over their mortgage lending as well.”

Taking a hands-on approach to supporting mortgage brokers who want to diversify, Westpac sits down with them for a meeting once they have shown an interest. They discuss their typical client base, their busi-ness model, and cover growth and networking strategies as well as educating the broker on what solutions the bank can offer.

For brokers who are still unsure about diversifying but are curious, the bank holds group and individual training.

“Our goal is to build long-term sustain-able relationships with our clients and brokers who are looking for expertise and a banker who understands their industry,” Pearce says.

“Business owners don’t have time to be repeating their story, so the brokers become the link and constant in a small business’s journey with Westpac Group.”

While securing finance at Westpac for home loans and SME business loans is similar in some ways, Pearce explains that there are a few differences.

“Instead of looking at a customer’s personal circumstances, we’re looking at their business circumstances. We need to understand the goals and aspirations of the business owner and how we can help them to achieve them,” she says.

“We will also need to review the financial background of the business and will assess the projected cash flow to help evaluate this. Having all their financial documentation current and available, such as business activity statements, bank statements, management accounts and personal tax returns, will help the small business owners prepare.”