Refinancing has kept the lending industry buoyed in the last 12 months, and it's not too late to help your customers save big on their home loans – with advice from these industry leaders

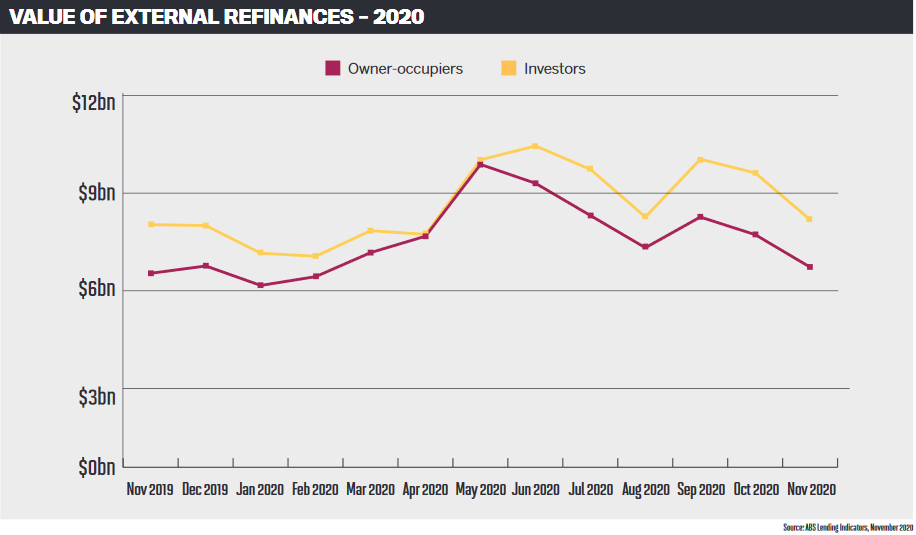

It's no secret that refinancing made up a huge portion of lending activity in 2020. Back in May, overall refinancing by owner-occupiers was worth around $15.2bn, with just under $10bn of that total value coming from borrowers who refinanced to a new lender. By comparison, in May 2019, external refinancing by owner-occupiers was worth just $5.7bn.

And that’s just the owner-occupier sector. Refinancing by investors peaked in June 2020, with over $8bn worth of loans refinanced.

So, why was refinancing so strong in 2020? Suncorp Bank head of broker partnerships Troy Fedder says that with the high economic uncertainty came an opportunity for borrowers to evaluate their finances and take advantage of historically low interest rates and refinance incentives.

“For some, 2020 was an opportunity to look for a better home loan deal with their broker or bank, while others took the opportunity to refinance their home and utilise equity for renovations,” Fedder says.

While customers usually choose to refinance as part of their strategy to meet their financial goals, Fedder explains, they may also be doing it to switch from a fixed to a variable rate, or vice versa, or for reasons beyond the financial.

“There are also other factors that come into play, with some borrowers looking for a lender who demonstrates social and corporate responsibility aligned to their values, or digital solutions which meet their banking needs,” he says.

Borrowers have also been refinancing to consolidate debts, such as credit cards, business loans and ATO debts, says James Angus, chief customer officer at Bluestone.

The non-bank in fact saw a drop in refinancing applications over 2020, due to its redirection towards prime lending, which has attracted much more purchase business. Still, refinancing made up 52% of all applications received by Bluestone.

“Refinancing can be an incredibly smart thing to do. When we think of the potential financial impacts of COVID-19, many households attempted to improve their cash flow via refinancing their home loan to a lower rate and consolidating high-interest unsecured debt,” Angus says.

Refinancing was not just important for customers who needed to save money or for keeping brokers busy – it kept the mortgage market active at a time when it could have really struggled. Resimac’s general manager, distribution, Daniel Carde said this surge of activity in the space introduced competitive pressure on interest rates, in turn benefiting borrowers with an unprecedented amount of choice of competitive home loan deals.

“Borrowers often refinance their home loans to take advantage of lower rates in the market – indeed, it’s one of the major benefits of choosing a variable interest rate over a fixed rate,” he says.

“But it’s not the only reason. Once borrowers have built up equity in their property, they can refinance their home loan and use that equity to finance things like home improvements, or to consolidate existing commitments.”

A budget reset for homeowners

A budget reset for homeowners

Refinancing is not a new thing, however; borrowers were choosing to do so long before 2020. But Mortgage Choice CEO Susan Mitchell says COVID-19 “reset the budgets of many households”. The broker group saw a 50% increase in refinancing submissions in the three months to May 2020, when compared to the same period one year prior.

Mitchell points out that the pandemic, the recession, RBA rate cuts and new government schemes would also have brought home loans to the forefront of consumers’ minds.

“Lockdowns and restrictions presented an opportunity to better realise the value of a home and, because it’s people’s biggest financial asset, refinancing their home loan made sense,” she says.

“Refinancing has always been an effective lead generator for brokers, but in 2020 our conversations with borrowers shifted from just getting a better interest rate to providing financial certainty and security in otherwise uncertain times.”

With a huge number of Australians working from home, this gave them time to not only look at their finances but also work on them, according to Pepper Money’s head of south east retail sales, Siobhan Williams.

“Many customers working from home found they had time to reassess their cash flow position and review their short- and long-term goals with their trusted advisers,” she says.

“Brokers have reported that their customers also found it easier to provide the necessary documentation, which supported a smoother application process.”

Working from home has also caused many more people to think about the properties they live in in a different way.

“We see borrowers who look to use their equity position for a whole range of purposes, including renovations,” Williams says.

“Renovations were a big driver in 2020 – borrowers were staying at home and buying more than just a sausage sandwich from Bunnings!

“We have also seen borrowers leverage equity to invest in their business and/or further property acquisition – both residential investment and commercial premises.”

Still a huge opportunity for brokers

Despite the rise in refinances, a recent RFi Group survey indicated that 72% of respondents had not refinanced their most recent home loan. This shows there was a huge opportunity for brokers to reach out to those customers who are missing out on savings.

ING’s acting head of retail, Glenn Gibson, says people’s circumstances change over time, and the home loan market is also constantly evolving.

“It can be helpful for brokers to conduct regular health checks to ensure their customers have the most suitable loans for their needs,” he says.

“Customers’ circumstances may change over time. They could have moved into a different life stage compared to the initial time they first got their home loan, and their needs would have also changed.”

Gibson warns that brokers who are helping their customers refinance should ensure they are matching the refinance to the right home loan.

“When it comes to comparing home loans, brokers should always try to compare apples with apples, and don’t forget to ask about the fees associated with moving loans, and the ongoing fees.

“It’s really important for brokers to understand the reasons why a customer wants to refinance, and sometimes a few thousand dollars cash back is not the right answer.”

Agreeing that customers could be refinancing for a range of financial or personal reasons, beyond interest rates and cash-back offers, Virgin Money’s head of distribution, Christian York, says brokers “play a crucial role” in continuing to understand customers’ circumstances and presenting them with options so they can decide which lender or product is most suitable for them.

“In addition, oftentimes customers may be turned off by poor experiences with the incumbent lender and want to look elsewhere,” York explains.

“Most brokers will develop long-lasting relationships with their customers and continue to touch base with them throughout the life of their loan to understand how their financial situation and goals change over time. Having these key conversations with customers is how the broker may discover a customer is interested in refinancing.”

Customers’ best interests in mind

To support the refinancing market, Suncorp has introduced its Easy Refinance initiative, which uses technology to access richer consumer credit information. This means the bank can identify applicants with a proven borrowing history, and those applicants who qualify will speed through the application process without having to provide as much documentation as customers who are applying for new home loans.

To support the refinancing market, Suncorp has introduced its Easy Refinance initiative, which uses technology to access richer consumer credit information. This means the bank can identify applicants with a proven borrowing history, and those applicants who qualify will speed through the application process without having to provide as much documentation as customers who are applying for new home loans.

Fedder reminds brokers who are helping customers to refinance that while lower interest rates over the long term may help save borrowers money, it is also important to disclose other factors that may apply to a refinance, such as fees or charges.

“With best interests duty top of mind for brokers, the break-even-point calculation when refinancing is likely key when deciding on a lending product, as well as consideration of loan features, the lender’s credit policy and current SLA,” he explains.

In light of this, brokers should also ensure they are considering the capabilities of non-bank lenders. Angus explains that non-banks like Bluestone do not have the restrictions on debt consolidation that the banks do.

For instance, Bluestone can consolidate up to $100,000 of unsecured debt under its prime home loan offering, whereas several banks are restricted to a small number of unsecured debts or have LVR and other restrictions, and some will not allow debt consolidation for self-employed borrowers.

Angus says brokers should stay in close contact with their existing customers and keep them abreast of refinancing opportunities.

“Take a deeper look at who your customers are and what they want; follow up frequently by providing something of value (for example, business insights and news through storytelling); keep customers abreast of new offers and, most importantly of all, create a service-focused culture in your business,” he says.

“I don’t believe there are any material risks in refinancing. Be aware of the interest rates available at the time of refinancing, take the time to understand each lender’s service proposition and turnaround times, and understand that you will ultimately pay for any cash-back offers. As the saying goes, there ain’t no such thing as a free lunch.”

Carde also warns brokers to watch out for cash-back offers and honeymoon rates, saying that for Resimac it’s about providing ongoing savings for the life of the loan. The non-bank also allows customers to make extra repayments, access the redraw and offset portions of the home loan, and pay off the loan early, which some banks do not.

Comparing a refinance application to a new home loan, Carde says there isn’t much difference, but there are key ways brokers can provide assistance, such as by making sure customers are aware of break fees that could negate any savings, and working out if they need lenders mortgage insurance.

“When chasing lower interest rates, it can be easy for borrowers to overlook all of the costs involved in refinancing a home loan,” he says.

“For a fixed rate home loan, break fees can be substantial. For those with less than 20% equity in their property, they will have to pay lenders mortgage insurance on the new loan as well. Both of these fees can vary dramatically, depending on each individual’s circumstances, and brokers are best positioned to help borrowers make an informed decision.”

Customers trust brokers over banks

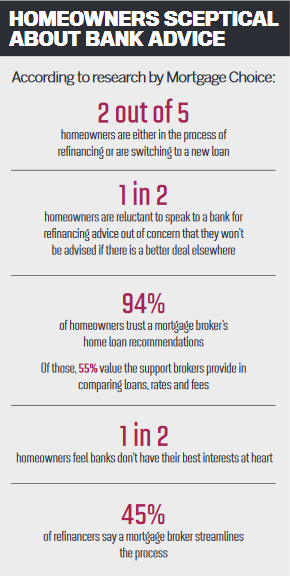

According to research from Mortgage Choice, 94% of homeowners trust a mortgage broker’s recommendation, and 53% are wary that if they speak to a bank they won’t be advised of better deals elsewhere.

Mitchell says refinancing isn’t always a black and white process, as lenders have different approval criteria for refinancers, and brokers are in a better position to navigate that landscape than borrowers.

“A good broker will be aware of any changes to a customer’s financial circumstances, as well as any change to house prices that will affect the use of equity in the home,” she says.

Mortgage Choice has kept its network of brokers across all the changes to policy, pricing and processes with weekly video updates, and has updated its technology and provided access to its lending advice forum.

“During the pandemic peak in April and May 2020, the Mortgage Choice customer communications team sent more than 1.5 million emails to existing broker customers and leads,” Mitchell explains.

“This was a deliberate strategy so that our customers were up to date with timely and professional information in what was otherwise an uncertain time, and so brokers could focus on what they do best.”

To ensure brokers and borrowers don’t have any surprises during the application process, Pepper Money recommends that brokers obtain a copy of the customer’s Comprehensive Credit Report before starting an application.

“Sometimes customers might forget they have had a late repayment or a dispute with their telco provider in the past,” Williams explains, adding that Pepper’s Product Selector Tool provides brokers with a free copy of their customer’s report.

Beyond that, Williams says brokers will need to spend time with their customers, identifying both their short-term and long-term needs.

“The solution presented will complement both,” she says. “If a customer is opting for a solution that will improve their cash flow today, they would be wise to speak to their broker or adviser about how to best utilise the savings. Extra repayments to the loan may put a customer in a better position to achieve those longer-term goals much sooner, whatever they may be.”

The importance of interest rates

RFi Group’s Australian mortgages research indicates that 69% of Australians would consider switching their mortgage to another institution that advertised a lower mortgage rate. However, 31% said they would not switch purely based on rate, emphasising the importance of other factors, such as fees and customer service.

While it seems likely interest rates will remain low in 2021, it is not certain how much longer this will continue.

“Interest rates are currently at an all-time low, so it’s highly possible we’ll continue to receive high volumes of people wanting to refinance,” ING’s Gibson says.“If borrowers haven’t reviewed their home loan interest rates, [and] in a few years there’s a change, they could be missing out on great savings.”

Virgin Money is also expecting to see refinancing remain a key source of market activity in 2021. But rather than being arguably the most important area of lending as it was in 2020, York says the first home buyer and investor segments will grow as well.

Brokers will therefore need to work closely with borrowers over the year ahead.

“Brokers need to ensure they have a clear understanding of their customers’ financial goals and objectives; this goes for all loans,” York says.

“Brokers are supported by their aggregators to adhere to industry compliance and regulatory reforms. There has been a huge amount of change, and brokers are in a fantastic position to provide their customers with education and support. Brokers are the core driver of our product in market, and we’re committed to working with our trusted network to deliver high-quality customer outcomes.”