As the challenges for SMEs trying to gain finance increase, six non-banks are providing alternative options

As the challenges for small businesses trying to gain finance increase, six non-banks are providing alternative options. They talk about their drive to help SMEs and how they are working with brokers to do so

MPA: What are the challenges currently facing small businesses?

Online lender OnDeck conducted research into small business customers and found that two out of five SMEs have sought finance in the past, but almost one in four have been knocked back by their bank.

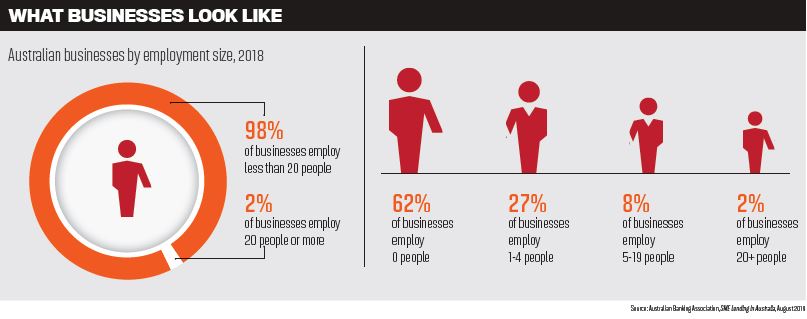

“Australian small businesses employ around 4.5 million Australians and account for 33% of private industry value add across Australian business – yet are often neglected by traditional lenders as being too risky or not asset rich enough,” says Michael Burke, head of sales at OnDeck Australia.

He adds that technology is changing the way the market thinks about business loans and this allows specialists like OnDeck to provide a solution to SMEs focusing more on cash flow and less on hard assets as security, while providing an easier, faster and better process.

For small business owners that require a loan, one of the main challenges is the type of documentation required to prove their revenue. While PAYG borrowers generally only require their two most recent payslips and personal bank statements, self-employed borrowers need more extensive documentation to assess the same types of loans.

“Self-employed borrowers applying for a loan through a mainstream lender usually require two years of tax returns, a notice of assessment from the ATO, and in some cases, their business bank records to show cash flow,” Royden D’Vaz, head of sales at Bluestone, says.

“Unfortunately, for many SMEs this is not always possible, for example if borrowers have not yet completed their latest returns or have traded for less than 24 months.”

Managing director at Equity-One, Dean Koutsoumidis, agrees that while running a small business has always had its challenges “perhaps today things are a little tougher”.

“Depending on the type of business, new technology-driven start-ups potentially can destabilise many of the once-familiar businesses which have enjoyed their long day in the sun,” he says of some of the general challenges facing businesses.

“Compliance challenges seem to be perpetually evolving, and the smallest and simplest of businesses still may find the compliance hurdles facing them quite a burden.”

It’s not all bad news; while the mainstream banks may have pulled back from certain areas of SME lending, all is not lost.

“Financing options have perhaps become somewhat less problematic, as there is now a plethora of new participants in the SME lending space,” Koutsoumidis says.

As well as being time-poor, Thinktank CEO Jonathan Street says this is combined with an uncertain economic outlook, weak consumer and business sentiment, and simple business survivability.

“There is a great deal of built up stress in the system at the present time and, while some are thriving, small business operators for the most part have a lot on their plate just to keep the doors open and continue to find ways to prepare for, and invest in, the future,” he adds.

He also acknowledges the difficulty small businesses are having with access to credit, most notably in accessing consumer finance, but says new entrants to the scene are a “welcome addition” to the market by placing customer experience and outcome at the forefront of their model.

Pepper

SMEs are nimble and dynamic, with the ability to move quickly to gain efficiencies or accelerate growth, but they can struggle to get access to capital to support their changing needs, says head of commercial Malcolm Withers.

“While in recent years we’ve seen an exciting growth in lenders in the SME space, we are also seeing traditional bank lenders become more restrictive in their approach to credit and slower in handling applications due to the recent regulatory reviews,” he says.

Believing that business owners are the backbone of the Australian economy, Liberty’s group sales manager John Mohnacheff says they take significant risks and are “crying out for business solutions”.

He says cash flow is a particular issue for smaller traders and Liberty has listened to this to provide a SME solution to help. The small business need for finance also provides a big opportunity for brokers.

“Brokers have an opportunity to help them get the finance they need, all while building a better relationship with the client for future transactions,” Mohnacheff says.

MPA: What are SMEs looking for when it comes to finance?

OnDeck

Off the back of its research, OnDeck sees that small businesses are spending too much time trying to organise bank funding. It found that 57% of SMEs had to slow or halt normal business activities while they waited for money and 40% were forced to delay debt payments.

Lenders like OnDeck are hoping to speed up the process. Burke says while it could take 4–6 weeks to get funding from the major banks, OnDeck aims to provide funding within three days. “In an increasingly competitive environment where Australian SMEs are competing in a global marketplace, this time saving can be the make-or-break factor that gives a business a competitive advantage,” he says.

Bluestone

Bluestone

D’Vaz agrees that time-poor business owners are looking for fast and convenient solutions. SMEs need finance for a range of purposes, including setting up a line of credit to assist with cash flow, purchasing business assets or consolidating ATO debt; so they need a flexible finance solution which meets all their needs.

“Because they often require funding to secure valuable business opportunities, an expedient turnaround on their application is critical,” he says.

As SME owners do not always fit into the standard documentation requirements, many are left looking for a lender who will assess them on a case-by-case basis and accept a wider range of documentation than a traditional bank, he adds.

Equity-One

Koutsoumidis says SMEs have always been looking for the same thing: “Quite simply, fast, cheap money. This hasn’t changed, really. Ever,” he says.

What is changing, however, is the market; Koutsoumidis observes there are more participants entering and the existing participants are broadening their offerings and searching for their own point of difference in the marketplace.

Taking a more positive view on the SME lending space than some others, he adds: “The supply of credit in this space is adequately meeting demand.”

Thinktank

All anyone wants when it comes to finance is a timely and acceptable solution which meets their needs, Street says; but all too often they are not getting it.

He breaks small businesses down into “two camps”: those that have been in an established and performing business, versus those that may be somewhere between a start-up and two to three years old.

With a high failure rate of small businesses in their first few years, the provision of credit, particularly unsecured, is a difficult proposition, Street adds.

“With access to credit more challenging than it has been in the best part of 30 years, lender credit appetite and policy constantly changing, product complexity only increasing and new lenders emerging regularly, timepoor business owners should be thinking ‘broker’ now more than ever,” Street says.

Liberty

Recognising the need for fast decisions, Liberty has placed an increased focus on that. “Our turnaround times are industry-leading,” Mohnacheff says. “We offer 24-hour turnaround times and direct access to underwriters so that brokers can be sure of a smooth and speedy process.”

To make things easier for brokers who are looking after small business clients, Liberty is building a dedicated business lending department to support the channel.

“We’re committed to helping more businesses to get financial with Liberty and this continues our unmatched record of innovation which will again lay a path for others to follow,” Mohnacheff adds.

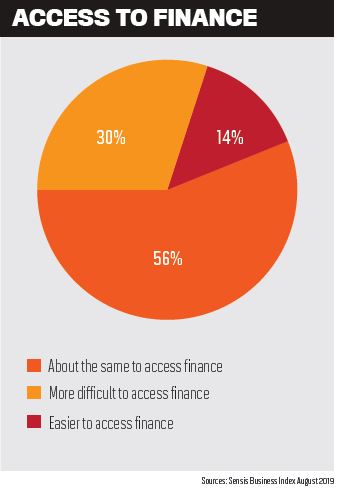

MPA: According to the Sensis Business Index, SMEs are finding it increasingly diffi cult to access finance. What are you doing to help these borrowers?

In the August 2019 Sensis Business Index, 30% of businesses in Australia said it was harder to access finance now than it was six months ago.

Bluestone

Recognising how time-poor business owners are, Bluestone is placing particular focus on turnaround times. This allows businesses to obtain the fi nance they need to take advantage of time-sensitive opportunities.

The lender recently put in place new policy changes designed to provide business owners with additional ways to prove their income for its near prime product.

D’Vaz says Bluestone also “stays away” from automated credit scoring, instead assessing each loan on a case-by-case basis.

“This helps us determine individual borrower needs a lot more accurately and supports positive customer outcomes for SMEs,” he says.

Equity-One

For Equity-One, helping business owners when they cannot get finance elsewhere is not a new thing. Koutsoumidis says that since its inception over 20 years ago, it has catered to small business owners and provided commercial finance when banks were not.

While he says this means Equity-One’s relevance in the market hasn’t really changed, there has been increased credit unavailability in the market recently with the major banks affected by the combination of APRA requirements and the flow-on effects from the royal commission.

“This has played well for alternative lenders, not just Equity-One,” he says. “Our loan offerings to SMEs are deliberately simple, because that’s all they need to be. We try to make access to commercial finance simple, as it should be.”

Thinktank

Understanding the growing complexity of the small business lending space, Street says it has never been a better time for brokers to help new and existing clients.

Thinktank is working closely with brokers to get the best outcome for their customers and is working with aggregator partners on a range of educational and business development events and sessions.

“Brokers don’t necessarily need to become experts in all areas but developing knowledge, confi dence and relationships with a range of lenders supported by experienced aggregator resources can mean the difference between a relatively static broking business and one where the first thing a client does when they have any type of finance need is call their broker,” he says.

Pepper

Pepper

The non-bank launched into the commercial space at the start of the year after brokers asked for an alternative commercial product to the banks. Withers says they have “reinvented the way commercial lending is done”.

Pepper’s offering “sits between the banks and the non-banks”, offering both full and alt doc loans, solutions for customers with tax debt, cash out requirements or credit impairments.

“In establishing Pepper Money Commercial, we wanted to be part of the solution for SMEs to access the funding they need,” Withers says.

“We recognise that brokers have a vital role in helping these businesses, which is why we developed a product that offers flexibility for both experienced or new-to-commercial brokers.”

Liberty

Understanding that even the more established businesses will still have cash fl ow worries, Liberty is piloting a new business loan called Liberty Lift. It offers loans of $25,000 to $1m for businesses with strong credit profiles which have been in operation for three years or more. Loan terms up to five years are secured by business cash flow and not a mortgage security.

“For the application we will need the businesses’ financial statements and completion of a streamlined application form,” Mohnacheff explains.

“We won’t require a mortgage for security against the loan, so the whole process is hassle-free and supported by Liberty’s leading service levels.”

MPA: According to the recent ABA SME Lending in Australia report, the smaller the business the more likely they are to seek out finance from a finance company over a bank – why do you think that is?

OnDeck

Burke says a significant development has been the growing awareness and interest in online lenders. OnDeck recently commissioned research which showed 22% of SMEs would consider an online lender: double the percentage of SMEs in the past.

“This is being driven partly by the mainstream banks and traditional lenders, as unsecured lending to small business is a market they don’t want to serve,” he says.

Bluestone

Much of the change is down to the realisation that non-banks and alternative lenders will offer solutions that banks won’t. They can assess each application on its individual merits, while traditional banks have a more rigid approach to assessment.

“In addition to this, business owners are usually time-poor and often need to secure funding very quickly, so they don’t lose valuable business opportunities,” D’Vaz says.

“Many non-banks are specifically set up to make the application and assessment process simple and turnaround time very fast, which makes them an easier and more efficient option for small business clients.”

Equity-One

Koutsoumidis agrees that turnaround times and ease are a big factor in why alternative lenders and non-banks are more attractive. “Banks are hot when they’re hot and not when they’re not,” he says. “Banks have become harder to deal with, and slow to get replies from. This isn’t good for business.”

Thinktank

Small businesses are turning more to nonbanks and other lenders partly because of the number of non-banks emerging squarely aimed at that particular part of the market, Street says, as well as the limited appetite from the banks. “In our view, the banks appear to be comfortable to hand over more market influence to the fintechs and non-banks who are proving to be more agile, technologically savvy and customer experience focussed,” he adds.

Pepper

Withers says he has observed over time that there is a growing gap between what a business client wants and what banks are able to provide.

On the one hand, there are SME clients who want a dedicated business banker: “Someone who understands their business and works with them to help them grow and navigate their finance needs,” he explains.

“On the other hand, you have the banks who are grappling with how to deliver this in a rapidly growing SME market. These clients are increasingly in need of a diverse range of lending needs, many of whom end up dealing with a bank call centre when they are expecting a personalised service.”

MPA: What do mortgage brokers need to know if they are considering moving into the SME lending space?

OnDeck

With the downturn in the residential property market, tighter restrictions for investor lending and the threat to commissions impacting the broker channel, the need for brokers to diversify beyond residential mortgages is highlighted, Burke says.

Diversifying may take brokers out of their comfort zone, but OnDeck is on hand to provide extensive support with its team of BDMs.

“OnDeck works closely with brokers during the first steps in the journey, providing training and sharing best practice. If the broker prefers, an OnDeck BDM can speak with customers directly on the broker’s behalf, though at all times the relationship belongs to the broker,” he adds.

Bluestone

D’Vaz says that SME loan applications are very similar to vanilla home loan applications, but that self-employed borrowers are more likely to require continuing fi nancial support compared to their PAYG counterparts, because their need for finance is often ongoing.

“The self-employed market offers a number of opportunities for brokers and moving into the SME lending space is a great fi rst step to diversifying your business as a broker,” he adds.

Equity-One

The SME market is a promising one, adds Koutsoumidis. “It provides brokers with an opportunity to deepen their relationship with their clients, broadening the cache of services they offer,” he says.

“This, ultimately, is good for their business as their connection with the client is deeper and more-sophisticated.”

Thinktank

Street says he has observed that the best and most effective SME brokers have a number of traits in common.

They are all client-focussed and maintain a regular discipline around contact to understand what their clients’ current needs are and what they might be in six to 12 months’ time and as far out as three or more years.

He also says they have great relationships with their aggregators, lenders and referral sources, and they are effective at making the most of their acquired experience to work through a deal.

“The most successful SME brokers thrive on their clients being comfortable that they obtained the finance that suited their needs and that in turn feeds strong repeat business and high conviction referral,” he adds.

Pepper

Reiterating the opportunity for brokers to expand their business beyond mortgages, Withers says “it allows brokers to have great customer conversations, get a deeper understanding of their customer, their plans and how they can support customers into the future with other products”.

“Remember, every self-employed client is a business owner so there is an opportunity for brokers to evolve into a business banking broker and provide the personal relationship a SME client is after.”

Liberty

As one of the biggest advocates for diversification, Mohnacheff reiterates the opportunities brokers have with SME clients.

He says brokers should look at their existing databases. “Residential brokers have a wealth of data to help them establish relationships with prospective SME clients,” he says.

“Reaching out to existing clients to let them know you lend in the commercial space allows a broker to build their experience within a network that already knows and trusts them.”