The opportunities for mortgage brokers to help their customers with vehicle finance continue to grow, but it is better to be cautious before jumping in at the deep end

For many, the idea of a home with a car in the driveway is a pretty simple one. However, not only are mortgages and vehicle loans the two largest expenses a customer will commit to, but often borrowers end up seeking out different finance professionals for help.

It is generally thought that most vehicle loans are obtained within the first six months of a new mortgage. So it makes sense that the borrower would benefit from using the same broker for both solutions.

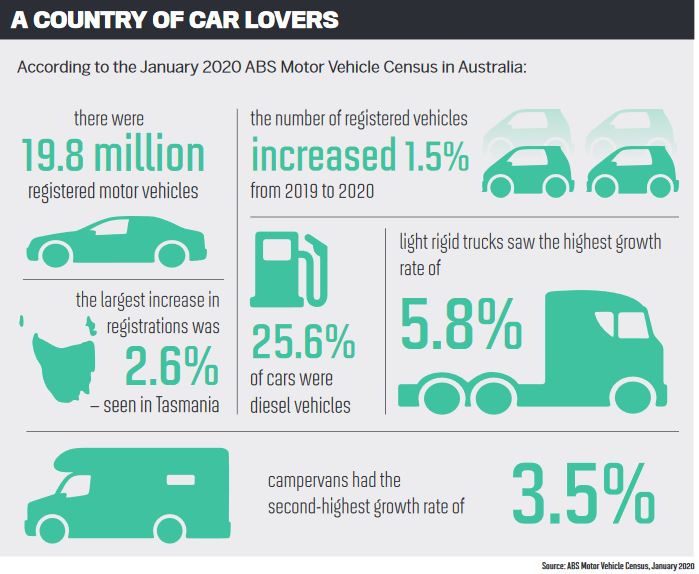

The opportunities extend beyond this. According to the ABS, there were 19.8 million registered motor vehicles as at 31 January 2020, and the number is increasing all the time, while more than 9.2 million households were recorded in the 2016 census. Almost 35% of those households held a mortgage.

One home loan for a broker could mean they could also help with two or three vehicle finance loans for the family.

Liberty’s group sales manager, John Mohnacheff, reminds brokers that people generally purchase cars much more often than they buy houses. He says brokers should always enquire about a mortgage borrower’s additional needs, because “you never know what you might uncover”.

“Investing a bit of time and effort in adding new products and services to your business can be incredibly rewarding,” he says.

It can be daunting to start with, however, and Mohnacheff says many brokers avoid trying other areas of lending because they are considered too difficult or complex. But he says that in fact very little changes.

“Succeeding in vehicle financing requires the same skills as it does in any other area of lending – and there is so much more opportunity for brokers who expand their customer offering,” he says.

While there are differences between loan size and asset type, a significant and not unwelcome difference is the speed of a vehicle finance deal. Where mortgage brokers can spend days or even weeks pulling a mortgage deal together, motor lending can happen within a few hours.

“In many ways, motor finance and mortgage broking complement each other. Vehicle finance can provide brokers with a steady stream of settled business while they support home loan customers over much longer time frames,” he says.

Liberty offers finance options for a range of vehicle types, as borrowers need finance for more than just new and personal cars. It offers fixed-rate car loans that can be used for new vehicles as well as those up to 20 years old and allows flexibility around loan terms and balloon repayments. The lender’s products also include business car loans, low-doc loans and custom out-of-the-box solutions.

“As private deals still constitute 60% of all used-car sales, it’s the perfect opportunity for mortgage brokers to get a message to their clients that they can assist them with finance for a private sale,” Mohnacheff adds.

Healthy demand spurs on brokers

Healthy demand spurs on brokers

Finance broker and principal and founder of Astute Ability Group Mhairi MacLeod has been offering vehicle and asset finance for more than 22 years. She started out as a business manager in a motor dealer before deciding to specialise as an asset finance broker running her own business. She services SME clients who usually need to finance several commercial vehicles.

MacLeod says offering vehicle finance as her core business proposition allows her to “deep-dive” into her self-employed SME customers’ needs and then in turn help their clients.

“One opportunity to finance an SME customer’s motor vehicle can potentially lead to a consumer personal loan for debt consolidation and home loan lending,” she says. “As a business, we’ve benefited by being able to cross-sell from one asset such as a car loan to various other assets in other industries, from excavators to six-wheeler trucks to a horse float or a shop fit-out.

“Offering vehicle finance gives brokers the opportunity to drill down into your client database and their connections on what needs and wants need to be filled.”

MacLeod’s time in the industry means she has seen it shift and grow, and one of the things she has noticed in particular is that the number of brokers diversifying or specialising in vehicle finance is growing.

“There has been an overall healthy market demand for vehicle finance, so it makes sense to see more brokers taking this opportunity to provide diversified solutions for their clients,” she says.

It’s not just brokers who are taking up the opportunities. MacLeod says it has been great to see more lenders entering the space and showing flexibility about each client’s needs, and there are also more support services for vehicle finance training.

Nevertheless, MacLeod warns that “diversification is not for everybody”. Her business understands the nuances and niches of vehicle finance, and her clients appreciate her specialty knowledge.

For example, her team know that clients need to repair or upgrade their vehicles, and this means they can help those clients with strategies to structure their finance in order to manage those costs.

“If you’re a mortgage broker and you’re already good at what you do, diversification into vehicle and asset funding will still require work and research,” she says.

“A vehicle finance deal is not simply a quick turnaround; it requires you to be agile and knowledgeable. You will need to be committed to learning and understanding the processes of vehicle finance, the different types of assets, different types of lending and different lenders’ policies. Start by considering which aggregators you choose to work with to access these lenders.”

Vehicle lending during COVID-19

Vehicle lending during COVID-19

Every industry has been affected in some way by the pandemic and the resulting restrictions, and motor vehicle finance is no different. Mohnacheff says it is facing challenges due the pandemic, but also because of changes to technology and customer expectations.

“The goal for us is to remain agile and innovative by adapting to these shifts so we can provide relevant products that support brokers and help more people to get financial,” he says.

In fact, the pandemic offers opportunities for brokers to look for alternative solutions. Mohnacheff says he has seen for himself and heard via word of mouth that there is a growing awareness of the options Liberty provides.

“During recent months, we have seen a growing number of brokers coming back to us for vehicle finance after experiencing how quick and seamless the process can be,” he says.

“Our dedicated motor BDMs are proactive in supporting and promoting to brokers the benefits of diversifying into vehicle finance.”

As a broker who has had to face these challenges, MacLeod says this year has changed the way the industry works and how individuals connect with each other.

“As for our clients, it’s business as usual, but we’re smarter about how we communicate with them: we’ve used a simple strategy of doing check-in calls with all our clients and asking them if there are any changes to their fi nances that they need assistance with,” she says.

“Also in this space, we’re acutely aware that SME business owners are more in need of tailored equipment finance funding, which we can provide.”