Many businesses are looking to grow in 2021 but are cautious about taking on more debt. Debtor finance could be the perfect solution

Research has highlighted the resilience of small businesses across Australia as more owners seek finance to invest and grow. But while Scottish Pacific’s SME Growth Index in March showed a strong bounce-back in business confidence, there were still concerns about the difficulty of accessing finance.

One in four businesses had cash flow issues after being declined for a lending product, one in five were planning to make arrangements with the ATO to manage their cash flow, and one in four SMEs were unsure of how they would recover.

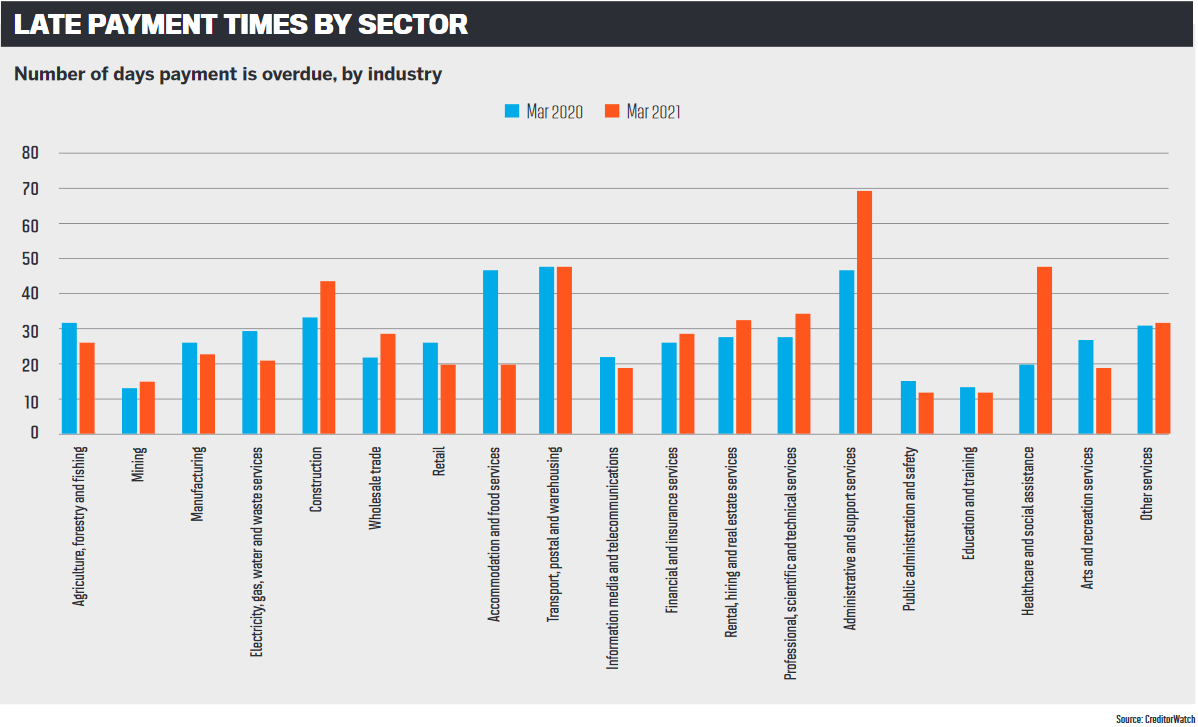

Figures from CreditorWatch show that one of the problems many businesses have had to navigate in the past year are lengthy payment times. Although business confidence is increasing, some industries are still in worse positions than they were a year ago in terms of overdue payments.

Hardest hit is the healthcare and social administrative services sector, which saw an increase of 140% in overdue payments from March 2020 to March 2021. Other badly hit areas are administrative and support services (+49%), construction (+29%), and professional, scientific and technical services (+25%).

Sectors that have seen a reduction in overdue payments are accommodation and food services (-57%), electricity, gas, water and waste services (-28%), retail (-23%) and manufacturing (15%).

One solution for these businesses is debtor finance, also called invoice finance, which is a type of funding that  boosts cash flow by giving businesses access to funds that would otherwise be tied up in their outstanding invoices.

boosts cash flow by giving businesses access to funds that would otherwise be tied up in their outstanding invoices.

“Unlike a loan, with debtor finance business owners don’t actually take on debt or have to make repayments; they in effect get early access to money they’ve already earned,” says Scottish Pacific senior executive Craig Michie.

“Debtor finance puts to work assets that are already in a business, giving owners peace of mind that their personal assets like the family home are not at risk.”

It provides a line of credit secured against trade receivables – the money a business is owed – and the business can access up to 95% of the value of their outstanding invoices. This allows business owners to take on new customers, invest in new equipment and staff, and negotiate better terms with suppliers as they have the cash to pay them earlier.

Businesses unwilling to take on new debt

Scottish Pacific’s SME Growth Index found that business owners’ intentions to fund growth in 2021 by using banks was at a record low, and their intention to use non-banks was at a record high.

Due to the uncertainty and business conditions brought about by COVID-19, Michie says small business owners did not want to take on more debt last year, and he expects this to continue in 2021.

“This debt reticence provided a great opportunity for many businesses to try debtor finance for the first time. Being able to fund opportunities using assets already in the business was an attractive drawcard for many SMEs in 2020 and remains so,” he says.

With business owners keen to get back to ‘business as usual’, demand has picked up and activity levels have risen over the past few months.

A big opportunity for brokers in the year ahead is in businesses looking to restructure. ScotPac’s SME Growth Index showed that two thirds of small businesses are making plans to restructure in 2021. In anticipation of increased demand, the non-bank is working with brokers and other advisers.

“The fact that 66% of small businesses plan to restructure is massive, and it provides a perfect opportunity for brokers to initiate discussions with their SME clients,” says Michie.

He encourages brokers to talk to their clients about the changes they are looking to make in the business, how this will impact their working capital needs, and their options for financing the business if there are shortfalls.

Many SME owners do not realise they can use business assets, such as stock, equipment, outstanding invoices and commercial property, to keep their family home out of the funding equation.

“Diversifying into working capital finance with ScotPac can open up many new opportunities for mortgage brokers, as we can fund their clients right through the supply chain using debtor finance and products such as asset finance (for equipment), progress claim finance and bad debt protection,” Michie says.

Debtor finance opens doors to more opportunities

Diversifying into debtor finance also provides brokers with additional revenue streams without the associated costs and upskilling that might come with financial planning.

Michie adds that helping businesses with debtor finance means the broker can then assist them further as they grow and look to purchase new equipment or property.

Unlike a mortgage application, there are no application forms to fill out, which means a broker can be as involved as they want to be. While there is a meeting to go over the financials, the broker can choose whether or not to be there, and whether or not they collect the financials and other details required, or leave it to the client.

Scottish Pacific provides training sessions, webinars and face-to-face events to help brokers understand the debtor finance market, as well as assess their clients. The non-bank is also currently beta-testing its new broker portal. Michie says the aim is to have approved lines of credit so that if a customer walks in needing $250,000 for their business, the broker can get a quick and simple approval.

“All our brokers really need to know is how to spot clients who may benefit from asset-based funding,” he says.

“Cash flow is the lifeblood of every SME. It can be hard for many small businesses to access bank funding – perhaps they haven’t got enough trading history, or don’t have or don’t wish to use personal property to secure business funding.

“From a single unpaid invoice to equipment or other business assets, these are ‘hidden’ assets a business owner might not even realise they have at their disposal, and we work with brokers to help their clients see this.”

As the economy continues its recovery and business owners look at how they can invest further, Michie says brokers will play an increasingly important role in helping them access funding.

He adds that it is important that brokers have conversations with their small business clients about how they can source funding to help them manage their cash flow, whether they’re looking for extra capital to replace JobKeeper funds, or to help them take advantage of growth opportunities.

“A final prediction is that the trend for small businesses to increasingly turn to non-banks, tracked since 2014 in our SME Growth Index, will continue and strengthen,” Michie says.

“This makes it a great time for mortgage brokers to take a look at diversifying their income streams by offering debtor finance and other asset-backed finance products to their clients.”