MPA hears from brokers on changes non-banks can make to engage consumers in our latest Brokers on Non-banks survey.

Brokers respond: What is the one change that could make consumers more likely to consider non-bank lenders?

MPA hears from brokers on changes non-banks can make to engage consumers in our latest Brokers on Non-banks survey. Here are some of the best responses:

• “There would have to be more brand awareness of that lender and who they are backed by. That goes to the public but I think more training to the third party needs to happen, to get customers comfortable.”

• “Have more BDMs on the road meeting with brokers and updating us on product and Policy niches so brokers are more confident selling product to clients. Sharing other brokers’ success stories and how they introduce non-bank lenders into the mix with the main banks. Try to be more price competitive with banks for AAA clients.”

• “Having easy access to the client’s information, having access points to the lender via general sales agents eg. Post Office. Focusing on regional locations as a go to for business (big banks are pulling away from regional lending) SERVICE, SERVICE, and SERVICE.”

• “I do think that non-banks are useful, especially in a changing market like the one we currently have. Clients are happy to go to a non-bank and follow broker advice but I really think that an online quick scenario form that gives all non-banks a crack at quoting and reply with policy concerns would help us all.”

• “The customer has to be assured that their initial interest rate will not be impacted by fluctuation of the market and the rate they went with initially becomes very uncompetitive over the next few months and they then want to refinance.”

• “Non-bank lenders need to increase brand awareness, not just of each non-bank lender, but of all non-bank lenders. To assist this ALL non-bank lenders should consider establishing a non-bank lender marketing body to plan marketing campaigns to increase brand awareness and the benefits of non-bank lenders.”

• “If all non-bank lenders were to join together and nominate one of the lenders with a good branch network to be able to deposit cheque’s and large cash deposits or even withdrawals it would give clients a quicker/ smoother loan process and also comparable service to the majors after the loan has settled.”

• “1) Change the term ‘Non-banks’(that word itself is a negative, as if lender lacks something because they are not a bank!) 2) Change perception that only Banks are ‘Safe’ ... Through media, rating agencies or the like.”

Consumers and the non-bank sector

Lack of consumer awareness is holding non-banks back, but brokers and pioneering non-banks have a number of solutions

Consumer awareness occupies an odd position in surveys about lenders. Ideally, when picking a product it shouldn’t matter at all; ‘marketing and brand awareness’ was brokers’ least important priority when picking a broker. However, for non-banks as a sector, consumer awareness, or lack thereof, is a major issue; in fact it’s the single most important reason for not putting more business through non-bank lenders, selected by 36% of respondents.

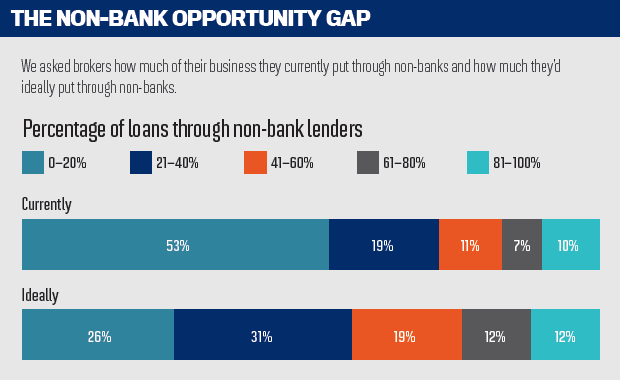

Here’s another notable statistic: 87% of our brokers said consumers would consider a non-bank product. Contrast that with the proportion of business that brokers actually put through non-bank lenders (see box). What this suggests is that non-banks don’t have an image problem; they’re not even being seen by consumers in the first place.

our brokers said consumers would consider a non-bank product. Contrast that with the proportion of business that brokers actually put through non-bank lenders (see box). What this suggests is that non-banks don’t have an image problem; they’re not even being seen by consumers in the first place.

It’s also notable that the proportion of brokers’ customers who would consider nonbank products hasn’t changed significantly since 2015 (when the percentage was 90%). With banks tightening criteria for investor lending, increasing interest rates for existing customers, and continuing to pull back from non-vanilla lending, you might presume this would increase, but then 90% is already a very high proportion. The challenge is converting consumer awareness into an increasing proportion of deals actually going to non-banks.

Brokers have put forward a range of excellent solutions to this challenge. Quite a few suggested a joint non-bank marketing drive to promote the sector – not an entirely unlikely situation, given credit unions and mutual currently cooperate through the Customer Owned Banking Association. Other respondents suggested more training of brokers; brochures illustrating non-banks’funding lines and comparing non-banks directly with banks; and even abolishing the term non-bank entirely. A few brokers suggested non-banks should target clients that banks have pulled back from, namely those in rural areas.

Another problem noted by brokers is consumer concerns over non-banks’ stability. One broker asked “to be able to provide them with something that demonstrates the strength of lender, so that it addresses the clients’ concerns on what happens to their loan if there was trouble in the mortgage market”. This extends to questions of price, the broker added, asking for “stats that show that the lender won’t increase rates down the track outside of Reserve Bank. They have concerns that what looks good now, may not be down the track. Making them feel comfortable and confident that they are ‘safe’”.

For non-banks that aim to flourish entirely through the third-party channel, this survey may provide cause for concern. It’s no coincidence that the top three non-banks in the survey – Homeloans, Liberty and Pepper – invest relatively heavily in marketing and brand awareness. As one broker put it, “brand awareness is a big one. Liberty has started to advertise on popular local radio stations and this made it very easy for me to discuss them and their services with my clients”. Homeloans sponsors the Perth Scorchers;Firstmac – which jumped to fourth place this year – sponsors the Brisbane Broncos; and Pepper gave their name to the Pepper Stadium in Penrith.

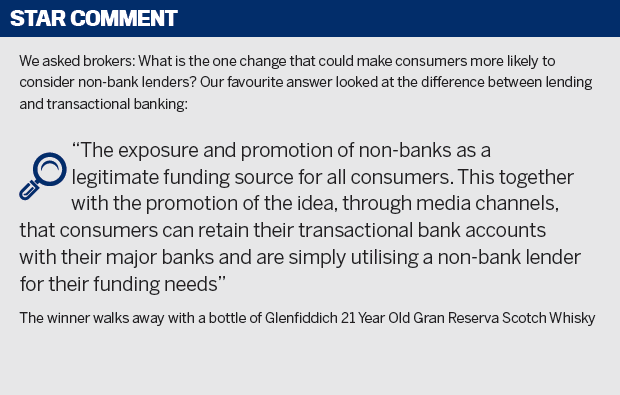

The problem for smaller lenders is the cost of traditional advertising and sponsorships. As Homeloans’ Ray Hair told MPA, this can be a challenge even for Homeloans. Social media is often touted as a low-cost solution, but this can be difficult in practice. Perhaps a joint social media effort could promote the message given by 2016’s ‘Star Commentator’ (see box): that consumers should feel free to use different financial providers for everyday banking and finance needs. That way non-bank lenders can get the level of business that their products and services deserve, without becoming just like the banks in order to do so.

MPA hears from brokers on changes non-banks can make to engage consumers in our latest Brokers on Non-banks survey. Here are some of the best responses:

• “There would have to be more brand awareness of that lender and who they are backed by. That goes to the public but I think more training to the third party needs to happen, to get customers comfortable.”

• “Have more BDMs on the road meeting with brokers and updating us on product and Policy niches so brokers are more confident selling product to clients. Sharing other brokers’ success stories and how they introduce non-bank lenders into the mix with the main banks. Try to be more price competitive with banks for AAA clients.”

• “Having easy access to the client’s information, having access points to the lender via general sales agents eg. Post Office. Focusing on regional locations as a go to for business (big banks are pulling away from regional lending) SERVICE, SERVICE, and SERVICE.”

• “I do think that non-banks are useful, especially in a changing market like the one we currently have. Clients are happy to go to a non-bank and follow broker advice but I really think that an online quick scenario form that gives all non-banks a crack at quoting and reply with policy concerns would help us all.”

• “The customer has to be assured that their initial interest rate will not be impacted by fluctuation of the market and the rate they went with initially becomes very uncompetitive over the next few months and they then want to refinance.”

• “Non-bank lenders need to increase brand awareness, not just of each non-bank lender, but of all non-bank lenders. To assist this ALL non-bank lenders should consider establishing a non-bank lender marketing body to plan marketing campaigns to increase brand awareness and the benefits of non-bank lenders.”

• “If all non-bank lenders were to join together and nominate one of the lenders with a good branch network to be able to deposit cheque’s and large cash deposits or even withdrawals it would give clients a quicker/ smoother loan process and also comparable service to the majors after the loan has settled.”

• “1) Change the term ‘Non-banks’(that word itself is a negative, as if lender lacks something because they are not a bank!) 2) Change perception that only Banks are ‘Safe’ ... Through media, rating agencies or the like.”

Consumers and the non-bank sector

Lack of consumer awareness is holding non-banks back, but brokers and pioneering non-banks have a number of solutions

Consumer awareness occupies an odd position in surveys about lenders. Ideally, when picking a product it shouldn’t matter at all; ‘marketing and brand awareness’ was brokers’ least important priority when picking a broker. However, for non-banks as a sector, consumer awareness, or lack thereof, is a major issue; in fact it’s the single most important reason for not putting more business through non-bank lenders, selected by 36% of respondents.

Here’s another notable statistic: 87% of

our brokers said consumers would consider a non-bank product. Contrast that with the proportion of business that brokers actually put through non-bank lenders (see box). What this suggests is that non-banks don’t have an image problem; they’re not even being seen by consumers in the first place.It’s also notable that the proportion of brokers’ customers who would consider nonbank products hasn’t changed significantly since 2015 (when the percentage was 90%). With banks tightening criteria for investor lending, increasing interest rates for existing customers, and continuing to pull back from non-vanilla lending, you might presume this would increase, but then 90% is already a very high proportion. The challenge is converting consumer awareness into an increasing proportion of deals actually going to non-banks.

Brokers have put forward a range of excellent solutions to this challenge. Quite a few suggested a joint non-bank marketing drive to promote the sector – not an entirely unlikely situation, given credit unions and mutual currently cooperate through the Customer Owned Banking Association. Other respondents suggested more training of brokers; brochures illustrating non-banks’funding lines and comparing non-banks directly with banks; and even abolishing the term non-bank entirely. A few brokers suggested non-banks should target clients that banks have pulled back from, namely those in rural areas.

Another problem noted by brokers is consumer concerns over non-banks’ stability. One broker asked “to be able to provide them with something that demonstrates the strength of lender, so that it addresses the clients’ concerns on what happens to their loan if there was trouble in the mortgage market”. This extends to questions of price, the broker added, asking for “stats that show that the lender won’t increase rates down the track outside of Reserve Bank. They have concerns that what looks good now, may not be down the track. Making them feel comfortable and confident that they are ‘safe’”.

For non-banks that aim to flourish entirely through the third-party channel, this survey may provide cause for concern. It’s no coincidence that the top three non-banks in the survey – Homeloans, Liberty and Pepper – invest relatively heavily in marketing and brand awareness. As one broker put it, “brand awareness is a big one. Liberty has started to advertise on popular local radio stations and this made it very easy for me to discuss them and their services with my clients”. Homeloans sponsors the Perth Scorchers;Firstmac – which jumped to fourth place this year – sponsors the Brisbane Broncos; and Pepper gave their name to the Pepper Stadium in Penrith.

The problem for smaller lenders is the cost of traditional advertising and sponsorships. As Homeloans’ Ray Hair told MPA, this can be a challenge even for Homeloans. Social media is often touted as a low-cost solution, but this can be difficult in practice. Perhaps a joint social media effort could promote the message given by 2016’s ‘Star Commentator’ (see box): that consumers should feel free to use different financial providers for everyday banking and finance needs. That way non-bank lenders can get the level of business that their products and services deserve, without becoming just like the banks in order to do so.