Brokers, lenders and experts speak out on what APRA’s tightening of investment lending could mean for you and your clients

For added context as the issue is still unfolding, please note this article was written for print in mid-June this year.

“PUT IT out! Put it out!” That’s one way you could summarise the Australian Prudential Regulation Authority’s urgent call to banks to cool down the overheated investor housing market in Sydney.

What set off APRA’s alarm bell was the hike in investor loan growth, which surpassed the 10% limit that the banking regulator had asked financial institutions to remain below late last year.

A quarterly study by APRA for March 2015 showed loans to investors had increased by 12.4% in the last 12 months, the sharpest rise in investor lending since September 2010.

Historically low interest rates only fuelled more investors to head to market, prompting an intervention from the banking regulator to put the brakes on residential property investor lending and, in turn, slow property price gains to reduce risk in the financial system.

What the big four are saying

Although changes to the lending environment have brought up speculation as to what the long-term repercussions may be, it’s only good news for brokers, according to Steve Kane, general manager of broker distribution for NAB Broker.

“It’s really the regulator saying that investor credit is growing, and they want to put restrictions on that, which are uniform across the industry,” Kane says. “This is not reflecting on brokers; it’s reflecting on the mortgage market and investors in particular. We believe that customers will use brokers because of the added complexity, so this will enhance the broker proposition because customers seek advice, as we can tell with over half of the market seeking advice from broking … we think that’s a real positive for broking.”

On whether upping the ante for investors will impact the broker-bank relationship, Westpac told MPA they don’t expect it will change, but aim to keep transparent communications with brokers going.

“We’ll continue to be open and transparent to ensure brokers not only understand the what, but we’ll give some context as to the reason why these things are happening,” says Tony MacRae, general manager for broker distribution. “We’ve always taken the approach that we’d treat both channels equally on this front.”

It’s important to remember that the bottom line comes down to the customer, explains Kieran Evans, ANZ’s head of third-party relationship channels.

“Ultimately, we are all striving for the same outcome – to deliver the customer the best home loan experience possible,” he says. “As the market continues to change and evolve, our focus is to keep our brokers informed as quickly as possible, and of course we’re focused on equipping our BDM team to help our brokers navigate any hurdles that come their way.”

Although Commonwealth Bank is making sure to stay below the 10% cap, general manager of broker sales Sam Boer says he’s keeping an eye on the effect it’ll have on the industry overall.

“I think there’s a lot of complexity,” he says, “and I’m a bit concerned about the potential impact it could have on the industry; for example, we saw what happened in 2006, when the NSW state government decided to introduce new taxes on investors, and it pretty much stalled that segment for a good few years. I don’t know how this is going to play out, so all we can do is ride it as it happens and adjust our business accordingly.”

The waiting game

The waiting game

Non-major AMP Bank is, in turn, watching what the other lenders are doing, says Glenn Gibson, head of sales and marketing.

“From a lender’s perspective, we’ve also got to understand what all the other lenders are doing because our growth could be impacted by the policies of another lender,” he explains. “The most important thing for us is simply a case of ‘wait and see’. Let’s see where everybody lands; let’s see what the market looks like and not be fearful of change – just look at it as another opportunity and understand where we can all grow our business from.”

In response to APRA’s actions, AMP has tightened investor lending by changing one of their assessment criteria for assessing repayment from 100% of rental income back to the standard 80%, in line with the majority of other lenders. They’ve also brought back onboard negative gearing.

“I think the hard policy changes are about to come across the different lenders, and we won’t see the impact of that until we start seeing settlements in about three months’ time,” Gibson told MPA in early June. “I think it’s going to be similar to pre-GFC. It’s always good to have a very strong blend of both owner-occupied and investor – you want to grow both investor growth and owner-occupied growth strongly for the growth of your mortgage book. So you tweak your polices and products to match what your blend is going to be, and I think that’s simply where we will end up – our blend will be different.”

Turning to non-banks

Turning to non-banks

With APRA exercising its regulatory sway over the banks and other regulated Authorised Deposit-taking Institutions, where do non-bank lenders stand?

Although La Trobe Financial sees the situation as a cyclical change only, they are ready for the major banks’ excess investment funding to potentially shift to non-banks.

“Our raison d’etre, since we began 63 years ago, is to service those borrowers who are underserved by the banks,” says chief lending officer Randal Williams. “While La Trobe Financial is not changing its policies with regard to investor borrowers, we have a very broad product range, and we will remain a very flexible option for investor borrowers.” The non-bank hasn’t noticed a significant increase in investment lending as of early June, but they expect investment lending to rise over the next six months as the APRA changes take effect.

Opportunity for brokers

MPA spoke to a number of brokers specialising in the investor space about how the banks’ reined-in policies for investment loans have impacted their brokerages.

Top 100 Broker Peter Gwynne of Choice Home Loans Varsity Lakes thinks the time is ripe to consolidate, given that the industry is experiencing the most significant changes since the GFC. “I want to consolidate, wait for the changes to come in and then look for opportunities” before the window of opportunity closes, Gwynne explains.

He suspects the changes are temporary. “I think greed will eventually take over like it always does, so there will be changes, but it seems to always float back to where it was before. If it slows it right down, it’s not going to be good for a lot of industries.”

John Manciameli, principal of Sydney brokerage Hunterwood Solutions, says he’s noticed clients are exploring areas for investment beyond Sydney and recognises the opportunity the crackdown has presented to brokers.

“I think this is the time where mortgage brokers are really going to add value to clients when you think about what they’re experiencing. They are seeing differences in interest rates for starters; there are differences in LVRs; there are differences in discounts being offered to investment property acquisitions. So for a mortgage broker, I think this is a wonderful time because this is where you’re really adding value to your clients’ property aspirations.”

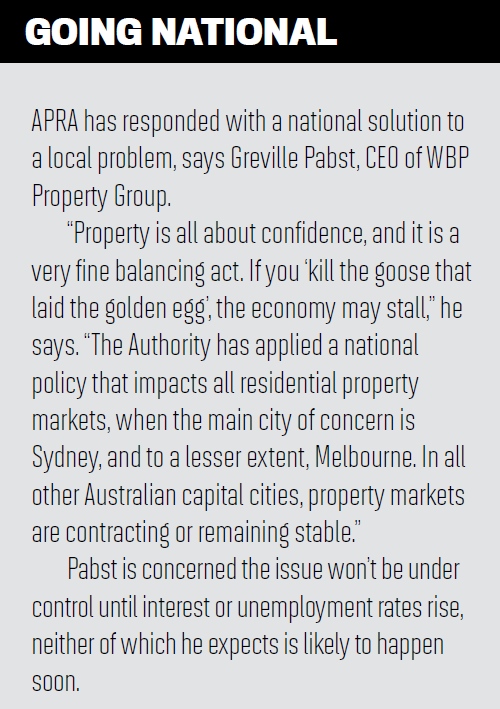

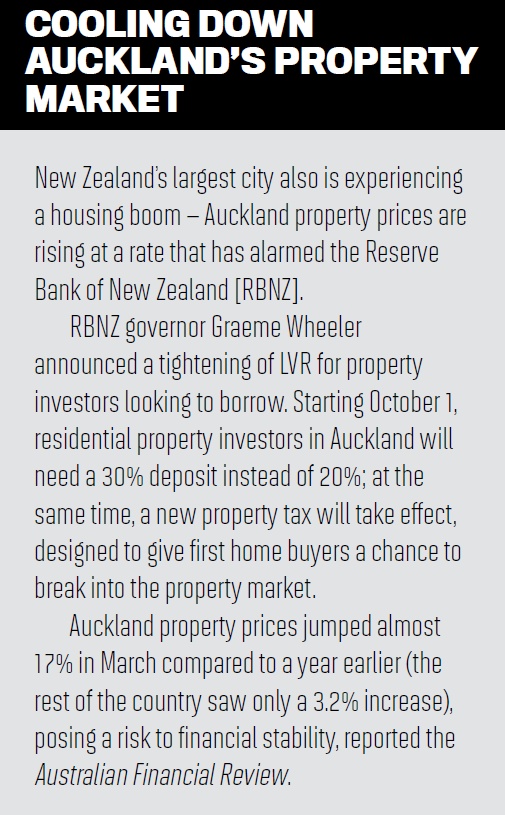

But, he adds, it’s baffling as to why the crackdown has extended to the entire country. “It’s really just a Sydney story – if you speak to someone in Perth, Adelaide, Darwin, their prices are dropping. They’re paying for all the excesses of Sydney, but it’s not even a big boom like in 2000 to 2004. It’s mind-boggling that they’re putting LVR restrictions and borrowing restrictions on the country. We should be looking to our cousins in New Zealand and saying, ‘Why don’t we put LVR restrictions on just Sydney’, like they’re doing in Auckland.”

“PUT IT out! Put it out!” That’s one way you could summarise the Australian Prudential Regulation Authority’s urgent call to banks to cool down the overheated investor housing market in Sydney.

What set off APRA’s alarm bell was the hike in investor loan growth, which surpassed the 10% limit that the banking regulator had asked financial institutions to remain below late last year.

A quarterly study by APRA for March 2015 showed loans to investors had increased by 12.4% in the last 12 months, the sharpest rise in investor lending since September 2010.

Historically low interest rates only fuelled more investors to head to market, prompting an intervention from the banking regulator to put the brakes on residential property investor lending and, in turn, slow property price gains to reduce risk in the financial system.

What the big four are saying

Although changes to the lending environment have brought up speculation as to what the long-term repercussions may be, it’s only good news for brokers, according to Steve Kane, general manager of broker distribution for NAB Broker.

“It’s really the regulator saying that investor credit is growing, and they want to put restrictions on that, which are uniform across the industry,” Kane says. “This is not reflecting on brokers; it’s reflecting on the mortgage market and investors in particular. We believe that customers will use brokers because of the added complexity, so this will enhance the broker proposition because customers seek advice, as we can tell with over half of the market seeking advice from broking … we think that’s a real positive for broking.”

On whether upping the ante for investors will impact the broker-bank relationship, Westpac told MPA they don’t expect it will change, but aim to keep transparent communications with brokers going.

“We’ll continue to be open and transparent to ensure brokers not only understand the what, but we’ll give some context as to the reason why these things are happening,” says Tony MacRae, general manager for broker distribution. “We’ve always taken the approach that we’d treat both channels equally on this front.”

It’s important to remember that the bottom line comes down to the customer, explains Kieran Evans, ANZ’s head of third-party relationship channels.

“Ultimately, we are all striving for the same outcome – to deliver the customer the best home loan experience possible,” he says. “As the market continues to change and evolve, our focus is to keep our brokers informed as quickly as possible, and of course we’re focused on equipping our BDM team to help our brokers navigate any hurdles that come their way.”

Although Commonwealth Bank is making sure to stay below the 10% cap, general manager of broker sales Sam Boer says he’s keeping an eye on the effect it’ll have on the industry overall.

“I think there’s a lot of complexity,” he says, “and I’m a bit concerned about the potential impact it could have on the industry; for example, we saw what happened in 2006, when the NSW state government decided to introduce new taxes on investors, and it pretty much stalled that segment for a good few years. I don’t know how this is going to play out, so all we can do is ride it as it happens and adjust our business accordingly.”

The waiting gameNon-major AMP Bank is, in turn, watching what the other lenders are doing, says Glenn Gibson, head of sales and marketing.

“From a lender’s perspective, we’ve also got to understand what all the other lenders are doing because our growth could be impacted by the policies of another lender,” he explains. “The most important thing for us is simply a case of ‘wait and see’. Let’s see where everybody lands; let’s see what the market looks like and not be fearful of change – just look at it as another opportunity and understand where we can all grow our business from.”

In response to APRA’s actions, AMP has tightened investor lending by changing one of their assessment criteria for assessing repayment from 100% of rental income back to the standard 80%, in line with the majority of other lenders. They’ve also brought back onboard negative gearing.

“I think the hard policy changes are about to come across the different lenders, and we won’t see the impact of that until we start seeing settlements in about three months’ time,” Gibson told MPA in early June. “I think it’s going to be similar to pre-GFC. It’s always good to have a very strong blend of both owner-occupied and investor – you want to grow both investor growth and owner-occupied growth strongly for the growth of your mortgage book. So you tweak your polices and products to match what your blend is going to be, and I think that’s simply where we will end up – our blend will be different.”

Turning to non-banksWith APRA exercising its regulatory sway over the banks and other regulated Authorised Deposit-taking Institutions, where do non-bank lenders stand?

Although La Trobe Financial sees the situation as a cyclical change only, they are ready for the major banks’ excess investment funding to potentially shift to non-banks.

“Our raison d’etre, since we began 63 years ago, is to service those borrowers who are underserved by the banks,” says chief lending officer Randal Williams. “While La Trobe Financial is not changing its policies with regard to investor borrowers, we have a very broad product range, and we will remain a very flexible option for investor borrowers.” The non-bank hasn’t noticed a significant increase in investment lending as of early June, but they expect investment lending to rise over the next six months as the APRA changes take effect.

Opportunity for brokers

MPA spoke to a number of brokers specialising in the investor space about how the banks’ reined-in policies for investment loans have impacted their brokerages.

Top 100 Broker Peter Gwynne of Choice Home Loans Varsity Lakes thinks the time is ripe to consolidate, given that the industry is experiencing the most significant changes since the GFC. “I want to consolidate, wait for the changes to come in and then look for opportunities” before the window of opportunity closes, Gwynne explains.

He suspects the changes are temporary. “I think greed will eventually take over like it always does, so there will be changes, but it seems to always float back to where it was before. If it slows it right down, it’s not going to be good for a lot of industries.”

John Manciameli, principal of Sydney brokerage Hunterwood Solutions, says he’s noticed clients are exploring areas for investment beyond Sydney and recognises the opportunity the crackdown has presented to brokers.

“I think this is the time where mortgage brokers are really going to add value to clients when you think about what they’re experiencing. They are seeing differences in interest rates for starters; there are differences in LVRs; there are differences in discounts being offered to investment property acquisitions. So for a mortgage broker, I think this is a wonderful time because this is where you’re really adding value to your clients’ property aspirations.”

But, he adds, it’s baffling as to why the crackdown has extended to the entire country. “It’s really just a Sydney story – if you speak to someone in Perth, Adelaide, Darwin, their prices are dropping. They’re paying for all the excesses of Sydney, but it’s not even a big boom like in 2000 to 2004. It’s mind-boggling that they’re putting LVR restrictions and borrowing restrictions on the country. We should be looking to our cousins in New Zealand and saying, ‘Why don’t we put LVR restrictions on just Sydney’, like they’re doing in Auckland.”