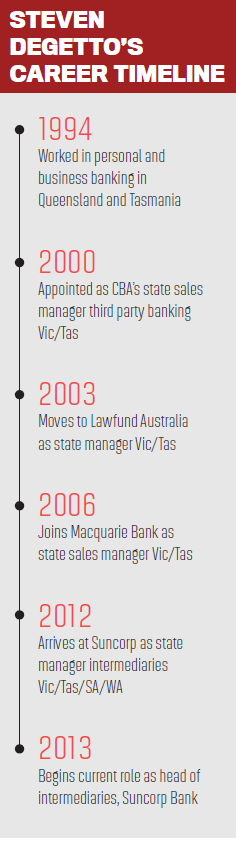

Suncorp’s head of intermediaries Steven Degetto tells MPA how he plans to keep the bank at the front of brokers’ minds.

Suncorp’s head of intermediaries tells MPA how he plans to keep the bank at the front of brokers’ minds.

MPA: Suncorp chose to raise interest rates in line with the majors. Does this mean you don’t see it as an opportunity to increase your market share?

Steven Degetto: If you look at interest rate changes there’s a whole bunch of things that we have to take into consideration: a highly competitive industry; regulatory costs increasing; we’ve got to balance customers and shareholders. Whilst we have raised rates … we’ve got some really competitive offers out there as well. Whilst we have increased variable rates by 0.16% we’re still in a really, really competitive position; the standard variable rate is now a benchmark rate, and what a customer is actually paying is different.

MPA: Does this mean an end to interest rate discounts on Suncorp’s owner-occupier products?

SD: Absolutely not. We’re really committed to helping customers achieve their financial goals. We’re about being the bank for aspiring Australians; you can absolutely count on us to continue delivering competitive offers to brokers who are open to trying lenders other than the majors, and who really look after their customers. We’ve got a track record of competitive offers to customers, and of giving brokers access to offers that they can present to their customers that they wouldn’t usually find.

MPA: Suncorp temporarily increased commissions on home loans to 0.75%. Should brokers get used to this level of commission?

SD: I think that commissions are continuing to come under scrutiny; you’ve seen in the life insurance industry that upfront commissions and sales commission have been capped, but interestingly they’ve been brought more in line with what is in the mortgage broking market now. In life

insurance you had 110 basis points commissions, and now they’re being brought back to the levels in mortgage broking.

I think there’s a balancing act with regulation. We’ve been a self-regulating industry from the start, and I think we need to stay conscious around commission levels. I think the key thing is putting customers’ best interests first, and most brokers absolutely do put customers’ best interests

first. Commissions are secondary or even an afterthought for most mortgage brokers. Certainly we don’t have any plans to permanently increase commissions, but last year we increased trail commission in year four, which was mainly to reward value. I think in the future you’ll see more lenders rewarding value and brokers who give us not just volume but value in their customers.

MPA: APRA has been pushing banks to control investment lending; how will Suncorp achieve this without alienating brokers?

SD: We’ve traditionally been focused more on owner-occupier lending, if you think about us helping people get ahead and being the bank for aspiring Australians. Our owner occupier customer base is significantly larger than our investor customer base. Having said that, people who are buying homes and wanting to get ahead often have investment properties, so for us it’s about being a responsible lender in that space and growing sustainably, being mindful of the regulators’ requirements. We’ll continue to manage our pricing in the market so we get the right mix, type and growth of lending mix.

MPA: In practical terms how has Suncorp invested in processing and improving turnaround times over the past year?

SD: In addition to the Ignite platform, we’ve recently rolled out a small business and commercial intermediaries team, within my team, and what we want to do is be the bank for small family businesses. Many aspiring Australians are self-employed, and we believe we can fill a void for those customers.

We’re working on two projects that you’ll see rolled out in 2016: there’s a new reward and recognition program for brokers; you’ll hear more about that in early 2016. We’re also working to further streamline our loan processing.

We’re Australia’s fifth-largest bank, and we’re one of Australia’s top insurers and Queensland’s largest company. We actually brought all of our insurance businesses under one project, and the same person who ran our insurance project is now running our banking project, so we’re able to leverage the group’s technological capability to benefit the bank, which we wouldn’t be able to do if the bank was on its own.

MPA: Who are Suncorp’s target clients, and has this profile changed in recent years?

SD: It has changed certainly. Over the last two years we’ve focused more on lower LVR and high-quality business. If you think about what aspiring Australians look like, it can be people buying their first home or looking to upgrade to their second home; people who might be renovating their property or expanding their business or buying their first or second investment property. It’s those people in the middle – we’re not about high risk and we don’t play at the fringes; we’re really about your everyday Australians who are looking to build a better future for themselves and their family.

MPA: Are brokers more willing to give non-majors a go than they were three years ago?

SD: I think it depends upon the broker, their own mindset, their experiences and where they might be in the cycle of their business. We find that there’s a whole bunch of brokers who are open to change … I certainly think we’ve built capability, we’ve built credibility; there’s a whole bunch of really great brokers out there who still are reluctant to go outside of their three or four key lenders. We’ve continued to lift the bar on our service levels, our competitiveness, our people, and we still need to continue lifting the bar on what our products look like.

We’ve got a highly rewarded Home Package Plus product; we’ve waived the annual package fee for the first year of the loan, and we’re really rewarding customers for bringing their whole banking to us. I think there’s still a bunch of brokers who don’t know what we’re about – and our job, and my team’s job, is to make sure we can have a seat at their table, so when they’re sitting across from their customer, we’re in consideration.

The broker value proposition is about choice, service and giving customers access to competitive offers and fantastic service. We believe we can deliver on that and we’d love for brokers to give us a chance to delight their customers.

MPA: How would you like Suncorp to be perceived 12 months from now?

SD: We want to be the standout genuine alternative for brokers and customers.

MPA: Suncorp chose to raise interest rates in line with the majors. Does this mean you don’t see it as an opportunity to increase your market share?

Steven Degetto: If you look at interest rate changes there’s a whole bunch of things that we have to take into consideration: a highly competitive industry; regulatory costs increasing; we’ve got to balance customers and shareholders. Whilst we have raised rates … we’ve got some really competitive offers out there as well. Whilst we have increased variable rates by 0.16% we’re still in a really, really competitive position; the standard variable rate is now a benchmark rate, and what a customer is actually paying is different.

MPA: Does this mean an end to interest rate discounts on Suncorp’s owner-occupier products?

SD: Absolutely not. We’re really committed to helping customers achieve their financial goals. We’re about being the bank for aspiring Australians; you can absolutely count on us to continue delivering competitive offers to brokers who are open to trying lenders other than the majors, and who really look after their customers. We’ve got a track record of competitive offers to customers, and of giving brokers access to offers that they can present to their customers that they wouldn’t usually find.

MPA: Suncorp temporarily increased commissions on home loans to 0.75%. Should brokers get used to this level of commission?

SD: I think that commissions are continuing to come under scrutiny; you’ve seen in the life insurance industry that upfront commissions and sales commission have been capped, but interestingly they’ve been brought more in line with what is in the mortgage broking market now. In life

insurance you had 110 basis points commissions, and now they’re being brought back to the levels in mortgage broking.

I think there’s a balancing act with regulation. We’ve been a self-regulating industry from the start, and I think we need to stay conscious around commission levels. I think the key thing is putting customers’ best interests first, and most brokers absolutely do put customers’ best interests

first. Commissions are secondary or even an afterthought for most mortgage brokers. Certainly we don’t have any plans to permanently increase commissions, but last year we increased trail commission in year four, which was mainly to reward value. I think in the future you’ll see more lenders rewarding value and brokers who give us not just volume but value in their customers.

MPA: APRA has been pushing banks to control investment lending; how will Suncorp achieve this without alienating brokers?

SD: We’ve traditionally been focused more on owner-occupier lending, if you think about us helping people get ahead and being the bank for aspiring Australians. Our owner occupier customer base is significantly larger than our investor customer base. Having said that, people who are buying homes and wanting to get ahead often have investment properties, so for us it’s about being a responsible lender in that space and growing sustainably, being mindful of the regulators’ requirements. We’ll continue to manage our pricing in the market so we get the right mix, type and growth of lending mix.

MPA: In practical terms how has Suncorp invested in processing and improving turnaround times over the past year?

SD: In addition to the Ignite platform, we’ve recently rolled out a small business and commercial intermediaries team, within my team, and what we want to do is be the bank for small family businesses. Many aspiring Australians are self-employed, and we believe we can fill a void for those customers.

We’re working on two projects that you’ll see rolled out in 2016: there’s a new reward and recognition program for brokers; you’ll hear more about that in early 2016. We’re also working to further streamline our loan processing.

We’re Australia’s fifth-largest bank, and we’re one of Australia’s top insurers and Queensland’s largest company. We actually brought all of our insurance businesses under one project, and the same person who ran our insurance project is now running our banking project, so we’re able to leverage the group’s technological capability to benefit the bank, which we wouldn’t be able to do if the bank was on its own.

MPA: Who are Suncorp’s target clients, and has this profile changed in recent years?

SD: It has changed certainly. Over the last two years we’ve focused more on lower LVR and high-quality business. If you think about what aspiring Australians look like, it can be people buying their first home or looking to upgrade to their second home; people who might be renovating their property or expanding their business or buying their first or second investment property. It’s those people in the middle – we’re not about high risk and we don’t play at the fringes; we’re really about your everyday Australians who are looking to build a better future for themselves and their family.

MPA: Are brokers more willing to give non-majors a go than they were three years ago?

SD: I think it depends upon the broker, their own mindset, their experiences and where they might be in the cycle of their business. We find that there’s a whole bunch of brokers who are open to change … I certainly think we’ve built capability, we’ve built credibility; there’s a whole bunch of really great brokers out there who still are reluctant to go outside of their three or four key lenders. We’ve continued to lift the bar on our service levels, our competitiveness, our people, and we still need to continue lifting the bar on what our products look like.

We’ve got a highly rewarded Home Package Plus product; we’ve waived the annual package fee for the first year of the loan, and we’re really rewarding customers for bringing their whole banking to us. I think there’s still a bunch of brokers who don’t know what we’re about – and our job, and my team’s job, is to make sure we can have a seat at their table, so when they’re sitting across from their customer, we’re in consideration.

The broker value proposition is about choice, service and giving customers access to competitive offers and fantastic service. We believe we can deliver on that and we’d love for brokers to give us a chance to delight their customers.

MPA: How would you like Suncorp to be perceived 12 months from now?

SD: We want to be the standout genuine alternative for brokers and customers.