Economics and demographics are bringing reverse mortgages back into the spotlight, and there’s a need for brokers to write them.

Demographic trends rarely make for a viable business strategy. For instance, we all know that Australia’s population is ageing, but how can you actually cater for older customers with no intention of changing properties? That’s where reverse mortgages come in.

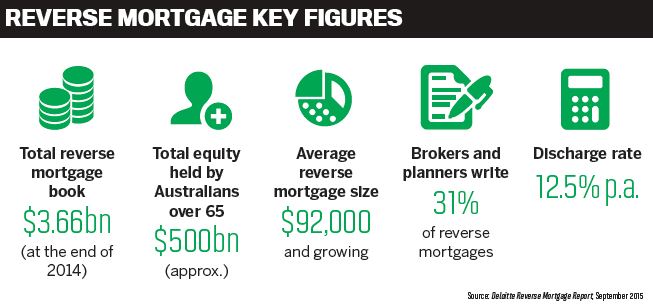

Reverse mortgages – which enable borrowers to release equity in their homes – have been brought back to prominence by an ageing population who want to stay in their homes, and by government policy and economics. By 2030, 3.6 million more Australians will be aged over 65 and thus eligible for reverse mortgages, according to CommBank, which has dubbed these customers ‘Peter Pans’. More immediately, the Coalition Government has already begun making changes to super pension rules, and most obviously, the cash rate is now at a historic low of just 1.5% and annual price growth has risen by 9% in Sydney and 7.2% in Melbourne.

Lenders are seeing the opportunity: the number of reverse mortgage providers has recovered substantially from a low point of five following the GFC.

For one of those lenders, Heartland Seniors Finance, potential reverse mortgage clients will look at brokers. CEO Andrew Ford says “brokers play a key part in mortgages and the mortgage market in Australia … brokers are the most valuable part of our distribution”. Accordingly, they’re making it easier to get accredited, putting their course and test online in October. Heartland has its own accreditation, while some providers require brokers to complete a course through Senior Australians Equity Release (SEQUAL), the industry association for providers of equity release products.

Reverse mortgages are an area in which advice is essential – indeed, independent legal advice is mandatory – and that’s why consumers want a broker’s assistance, says Darren Moffat, managing director of Seniors First. “In some respects it’s a simple product, but it also has lots of implications if handled incorrectly. Seniors like to have someone guiding them through the process, particularly around product selection and lender selection.”

“Seniors like to have someone guiding them through the process, particularly around product selection and lender selection” Darren Moffat, Seniors First

Moffat, who’s based in Sydney, has been writing reverse mortgages since 2005. He’s seen the sector undergo two rounds of regulation – the NCCP in 2010 and more specific regulation in 2011 – but doesn’t believe it’s made his job much harder.

“There is more paperwork, but if you were doing the right thing beforehand you wouldn’t find it onerous; certainly we haven’t,” he says.

Like some other brokers, Moffat views increased regulation as an encouraging development. However, Peter Bolitho, director of Reverse Mortgage Finance Solutions on the Sunshine Coast, who’s been working with reverse mortgages for over 20 years, notes there’s “definitely been more regulation, but there are areas of regulation which still cause me some concern”.

Reverse mortgage clients come to Bolitho through referrals from branches, other brokers and increasingly through the company’s website as older people make more use of the internet.

Brokers should take note of who’s making the application, he warns. “My concern is when you have a son or daughter making an application on behalf of their parents, the danger of elder abuse is too great, I think.”

Brokers and lenders need to make sure that the funds will primarily benefit their borrower, but “without face-to-face contact it’s very difficult to establish that”.

Brokers and lenders need to make sure that the funds will primarily benefit their borrower, but “without face-to-face contact it’s very difficult to establish that”.

Heartland Seniors boss Ford says brokers should feel comfortable writing reverse mortgages. “We’ve got a really robust and thorough fulfilment process which includes independent legal advice and gets the customer to talk to their family – and attest to the fact they have.”

Among other safeguards ‘hard coded’ into the product is the obligation to give the borrower a loan projection using ASIC’s calculator, and to explain alternatives – whether the borrower would be better off downsizing, or borrowing from friends and family – as well as how a reverse mortgage could impact on their pension and inheritance. With oversight from the broker, lender, client’s solicitor and possibly a financial planner, “if there’s something that consumers are uncomfortable with it’s going to be discovered somewhere along the line”, says Senior First’s Moffat.

The timeframes involved in reverse mortgage lending can be incredibly diverse.

While lenders’ turnaround is typically a couple of weeks – longer if refi nancing is involved – the main delay is the client’s decision time: unlike buying a new house, there is no ‘trigger’ for reverse mortgage borrowers, explains Bolitho. There can be triggers – the client running out of money due to a car breakdown, for example – although these are generally preceded by the client researching reverse mortgages as a solution. At Seniors First, Moffat finds the client’s decision-making time is typically six to eight weeks (although his longest client took seven years); Bolitho’s figure is four to six weeks.

While lenders’ turnaround is typically a couple of weeks – longer if refi nancing is involved – the main delay is the client’s decision time: unlike buying a new house, there is no ‘trigger’ for reverse mortgage borrowers, explains Bolitho. There can be triggers – the client running out of money due to a car breakdown, for example – although these are generally preceded by the client researching reverse mortgages as a solution. At Seniors First, Moffat finds the client’s decision-making time is typically six to eight weeks (although his longest client took seven years); Bolitho’s figure is four to six weeks.

Many elements of applying for a reverse mortgage will be familiar to brokers: submitting paperwork, credit approval and receipt of funds. When deciding which product, however, there are a couple of details to watch out for. The interest rate is crucial, given many lenders won’t require any payments and thus interest gets compounded. Regular fees should also be watched out for, for the same reason – Moffat says he tries to avoid them – and the LVR may be crucial to the client if they’re looking to get as much money out as possible.

In terms of conditions, there is some differentiation among lenders. Since 2012 the law has stipulated that reverse mortgage borrowers can never owe more than their house is worth. At Heartland Seniors they also guarantee clients lifetime occupancy, explains Ford, and allow partial or full repayment at any time without a penalty. Some lenders allow flexibility as to whether they receive the funds as a lump sum, a line of credit or a regular for brokers. Most brokers cover the gap with a fee, explains Bolitho. “I believe that the majority of brokers in this area now charge a fee-forservice, which is discussed with and divulged to the client, because it’s the only way you can maintain a specialisation in this area.” Clients rarely take issue with a fee, he adds. “I’ve had probably one client in the last five years that complained about it. Clients understand that, as long as they’re getting that level of service.”

“I’ve had probably one client in the last five years that complained about [fees]. Clients understand that, as long as they’re getting that level of service” - Peter Bolitho, Reverse Mortgage Financial Solutions

Reverse mortgages, it should be noted, typically stay on the books for longer and increase as clients draw out extra funds, meaning that over the long term they can form an important part of a broker’s book. Furthermore, for Moffat, writing reverse mortgages is a ‘feel-good experience’. “You’re actually helping people: these loans have a very significant impact on people’s lives. That aspect of the work shouldn’t be underplayed; it’s why we do what we do.”

There’s another reason: necessity. As Moffat concludes, “this [over 60s] demographic is the fastest-growing part of the population; reverse mortgages provide a great opportunity for brokers to tap that part of the market … over the next 10 years you’re going to see this part of the market grow very rapidly.”