MPA looks at the risk involved in broker-sourced loans and why lenders continue to advocate for the channel.

APRA chairman… higher default rates and risk… third-party originated loans… sound familiar?

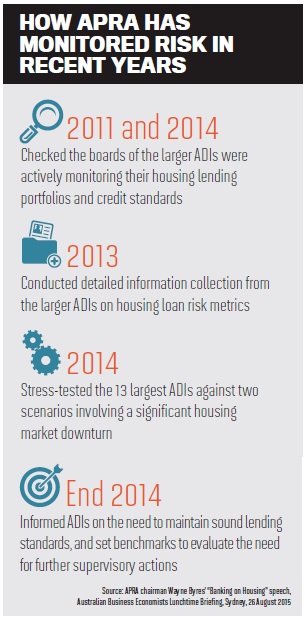

You may recall the stir caused among brokers when APRA chairman Wayne Byres warned lenders about third-party originated loans at the Australian Business Economists briefing in August.

Byres said, “Third-party originated loans tend to have a materially higher default rate compared to loans originated through proprietary channels.”

The regulator gave MPA an insight into its data on default rates, which it had requested from a number of the largest lenders. Its spokesperson said: “This data showed that the default rate on mortgages originated through third-party channels was typically higher than mortgages originated via proprietary channels. There were differences from lender to lender but, on average, the average default rate for third-party originated loans was around 30% higher.”

But despite highlighting higher default rates on third-party loans, the chairman went on to say at the briefing: “This does not mean third-party channels have lower underwriting standards, but simply that the new business that flows through these channels appears to

be of higher risk, and must be managed with appropriate care.”

However, the mention of higher default rates and higher risk associated with third party loans gave brokers cause for concern that their loan-writing abilities and the quality of broker-sourced loans were being negatively portrayed, leading the industry associations

to question APRA’s comments.

MFAA CEO Siobhan Hayden was able to meet with APRA and clarify for the industry that Byres’ comments on the riskier nature of third-party loans were not an attack on brokers’ loan-writing abilities.

“It was more around that the type of customers that would present themselves to a teller versus the type of customers that would engage with a finance broker – [they] are different, and inherently I would agree with that,” Hayden told MPA. “The types of structures that finance brokers are asked to support customers on are more detailed, more involved and require more consideration, so I didn’t disagree with that analysis.”

She said APRA did suggest very clearly to her that the overall rate of arrears and defaults was negligible – the lowest it had been in this economic climate. Another positive outcome was that the association was also able to provide more details to the regulator on how APRA’s decisions affect the broker channel directly.

Clearing up areas of confusion such as these is one of the reasons associations are invaluable to brokers and their industry as a whole.

“You need the industry body to be able to be there having that dialogue [with APRA or ASIC], and this is one of the most important things that associations do,” said FBAA chief executive Peter White. “This is where industry associations are at their fore.

“Normally it’s not a regulator that we deal with; they don’t regulate our industry. At the end of the day APRA is looking at the credit and regulatory regime of the lenders and they’re looking at their processes and credit policies – a broker can’t write a loan that isn’t within credit policy.”

MPA took a look at what other statistics had to reveal about third-party originated loans, and what lenders, a risk expert and an aggregator had to say on the quality of broker introduced loans.

The MFAA’s 2015 Ernst & Young report Observations on the Value of Mortgage Broking found there was no difference between thecredit quality of the retail and broker channels. “There has not been any material differences witnessed in the characteristics (ie credit quality, cost of acquisition (post commissions), net interest margin and loyalty) of the broker portfolio to that of proprietary channels,” the report stated.

“With regards to credit quality, lenders noted that the arrears rate in both portfolios is largely similar. It should be noted however, that given the historically low levels of arrears lenders are experiencing this has only been analysed by lenders at a headline level.”

One thing that is certain is the broker market share is only going up. The MFAA’s 2015 report states that broker-originated loans now contribute to 50% of mortgages in the system (both new and refinanced), double the volume since 2003 when around 25% of all new home loans were sourced through brokers, according to the Reserve Bank’s 2004 Financial Stability Review.

Risk management expert Professor Paul Kennedy of Macquarie University said the fact that broker-originated loans involved extra participants gave them a tendency to be riskier.

“Every layer you put in the financial process gives you more challenge in getting the incentives right and making sure everything is aligned to a fair and equitable outcome,” Kennedy said.

‘I think [broker-originated loans] bring their own challenges, and the challenges include they are one step removed from the lender, so you need to ensure that you have strong connection and oversight with them – also, the population of people that they are dealing with may be different from those who come directly to the lender themselves.

“You need different channels to ensure you can service the market. Different channels come with their own particular challenges. Those are not insurmountable challenges; you just need to be aware of them when you are growing that channel.”

WHY AUSSIE BROKERS RANK HIGHLY ON COMPLIANCE ON GLOBAL STAGE

The risk involved in broker introduced loans within Australia compares well with those originated by brokers globally, says Professor Paul Kennedy of Macquarie University. With extensive experience in risk management at top banks in Europe and Australia, among them CBA and NAB, Kennedy says historically Australian brokers have compared quite well.

“Although Australia has suffered incidents of, for instance, poor broker-originated loans, they tend to be restricted to specific firms and regions,” he says.

“I think Australia’s had isolated poor incidents which are intrinsic to the business model, and there will always be the odd bad apple, but so far we have escaped the worst systemic abuse that has been perhaps a bit more obvious particularly in the UK. We actually have a reasonable financial system and I think we’ve been tested quite well through the global financial crisis in comparison – our financial system is pretty sound.”

Brokers’ top priority

That most brokers in the industry want to achieve high compliance and do the best by their clients is probably fair to say.

“I think brokers have a very real concern that they are compliant with the law. I would say it’s probably on the top of mind with just about every broker that I speak to,” said Vow CEO Tim Brown, who explained that their compliance webinars were the best attended of all of Vow’s webinars.

One of Australia’s largest aggregation groups, Vow has a strong presence in compliance training for its brokers and runs a broker survey every six months. “Compliance is our most highly regarded area,” says Brown. “Our compliance area gets a 93% satisfaction rating, which shows they really value the education that we give them through our compliance.”

The aggregator also runs workshops that give brokers the opportunity to bring in their own files and discuss them. “People are able to have an open discussion without feeling threatened that they are going to get caught out. We find, educationally wise, they learn more from that experience than by us going and doing audits.”

While compulsory for those under Vow’s licence, brokers are finding the workshops so useful that those with their own licences are requesting that the aggregator runs similar workshops for a fee.

“They’ve been requesting that they want to attend our workshops, and they want us to do audits on them. It would give us some comfort, too, to know they are being compliant, albeit they’re not under our licence.”

Brown’s background in banking has placed him in a good position to compare the retail and broker channels.

“Most brokers have been in the industry a long time; they tend to have come out of major banks and so they tend to be well trained anyway and they know what not to do. They’ve got integrity and they know that their licence can be put at risk if they put a client into a loan that they can’t afford or that isn’t the right product for them.”

Broker-originated lending stands tall

MPA spoke to three lenders, who explained why the future was looking bright for the broker channel – and said third-party originated loans were ticking all the boxes.

Australia’s largest customer-owned bank, Heritage Bank, sources 50% of its mortgage loans through brokers and 50% from its retail network. The bank has also had an exceedingly strong year in loan origination through its broker partners, head of third party channels David Ure said. “This channel gives us access to markets across Australia,” he said. “Our relationship with the channel is considered very important.”

Ure said the bank’s main risk associated with loans introduced through a third party was in receiving/assessing and approving loan applications. “However, this risk is well mitigated through legislation and compliance requirements within the industry, as well as Heritage’s relationship with our broker partners,” he said.

But for ING Direct head of broker distribution Mark Woolnough, brokers don’t introduce any material risk into the process. “We’ve been working with brokers for a long time, nearing 20 years now, and we’ve always said to brokers and internally, they are essentially an extension of our own sales team. Being a branchless bank we don’t have a face-to-face or mobile sales network. We see our broker partners as the extension of our sales force, and therefore they’re effectively seen as our shopfront.”

He said brokers accounted for more than 20% of ING Direct’s lending business and there was no significant difference regarding approvals, defaults or refinances between direct and broker customers. “For us, there’s no statistical difference because our focus is not on just getting people into their homes but to make sure they stay in their homes longterm, which is reflected in where we pitch our products and our credit policy and our appetite to help customers.”

ME’s general manager brokers Lino Pelaccia said his bank’s experience of working with brokers had been “extremely positive”, with half of ME’s home loan sales originating from brokers in the past year.

“Brokers run professional, risk-averse businesses that are compliant and accredited with industry bodies,” said Pelaccia. “Brokers are also a great source for instant feedback on the state of the market and how our products and services are being received.”

ME plans to expand its broker network and expects it to generate 55% of home loan settlements over the next three years, totalling $3.3bn in FY16 and increasing to $5.3bn in FY18. “Brokers are a valued sales channel for ME, and the broker channel is critical to our growth plans going forward.”

You may recall the stir caused among brokers when APRA chairman Wayne Byres warned lenders about third-party originated loans at the Australian Business Economists briefing in August.

Byres said, “Third-party originated loans tend to have a materially higher default rate compared to loans originated through proprietary channels.”

The regulator gave MPA an insight into its data on default rates, which it had requested from a number of the largest lenders. Its spokesperson said: “This data showed that the default rate on mortgages originated through third-party channels was typically higher than mortgages originated via proprietary channels. There were differences from lender to lender but, on average, the average default rate for third-party originated loans was around 30% higher.”

But despite highlighting higher default rates on third-party loans, the chairman went on to say at the briefing: “This does not mean third-party channels have lower underwriting standards, but simply that the new business that flows through these channels appears to

be of higher risk, and must be managed with appropriate care.”

However, the mention of higher default rates and higher risk associated with third party loans gave brokers cause for concern that their loan-writing abilities and the quality of broker-sourced loans were being negatively portrayed, leading the industry associations

to question APRA’s comments.

MFAA CEO Siobhan Hayden was able to meet with APRA and clarify for the industry that Byres’ comments on the riskier nature of third-party loans were not an attack on brokers’ loan-writing abilities.

“It was more around that the type of customers that would present themselves to a teller versus the type of customers that would engage with a finance broker – [they] are different, and inherently I would agree with that,” Hayden told MPA. “The types of structures that finance brokers are asked to support customers on are more detailed, more involved and require more consideration, so I didn’t disagree with that analysis.”

She said APRA did suggest very clearly to her that the overall rate of arrears and defaults was negligible – the lowest it had been in this economic climate. Another positive outcome was that the association was also able to provide more details to the regulator on how APRA’s decisions affect the broker channel directly.

Clearing up areas of confusion such as these is one of the reasons associations are invaluable to brokers and their industry as a whole.

“You need the industry body to be able to be there having that dialogue [with APRA or ASIC], and this is one of the most important things that associations do,” said FBAA chief executive Peter White. “This is where industry associations are at their fore.

“Normally it’s not a regulator that we deal with; they don’t regulate our industry. At the end of the day APRA is looking at the credit and regulatory regime of the lenders and they’re looking at their processes and credit policies – a broker can’t write a loan that isn’t within credit policy.”

MPA took a look at what other statistics had to reveal about third-party originated loans, and what lenders, a risk expert and an aggregator had to say on the quality of broker introduced loans.

The MFAA’s 2015 Ernst & Young report Observations on the Value of Mortgage Broking found there was no difference between thecredit quality of the retail and broker channels. “There has not been any material differences witnessed in the characteristics (ie credit quality, cost of acquisition (post commissions), net interest margin and loyalty) of the broker portfolio to that of proprietary channels,” the report stated.

“With regards to credit quality, lenders noted that the arrears rate in both portfolios is largely similar. It should be noted however, that given the historically low levels of arrears lenders are experiencing this has only been analysed by lenders at a headline level.”

One thing that is certain is the broker market share is only going up. The MFAA’s 2015 report states that broker-originated loans now contribute to 50% of mortgages in the system (both new and refinanced), double the volume since 2003 when around 25% of all new home loans were sourced through brokers, according to the Reserve Bank’s 2004 Financial Stability Review.

Risk management expert Professor Paul Kennedy of Macquarie University said the fact that broker-originated loans involved extra participants gave them a tendency to be riskier.

“Every layer you put in the financial process gives you more challenge in getting the incentives right and making sure everything is aligned to a fair and equitable outcome,” Kennedy said.

‘I think [broker-originated loans] bring their own challenges, and the challenges include they are one step removed from the lender, so you need to ensure that you have strong connection and oversight with them – also, the population of people that they are dealing with may be different from those who come directly to the lender themselves.

“You need different channels to ensure you can service the market. Different channels come with their own particular challenges. Those are not insurmountable challenges; you just need to be aware of them when you are growing that channel.”

WHY AUSSIE BROKERS RANK HIGHLY ON COMPLIANCE ON GLOBAL STAGE

The risk involved in broker introduced loans within Australia compares well with those originated by brokers globally, says Professor Paul Kennedy of Macquarie University. With extensive experience in risk management at top banks in Europe and Australia, among them CBA and NAB, Kennedy says historically Australian brokers have compared quite well.

“Although Australia has suffered incidents of, for instance, poor broker-originated loans, they tend to be restricted to specific firms and regions,” he says.

“I think Australia’s had isolated poor incidents which are intrinsic to the business model, and there will always be the odd bad apple, but so far we have escaped the worst systemic abuse that has been perhaps a bit more obvious particularly in the UK. We actually have a reasonable financial system and I think we’ve been tested quite well through the global financial crisis in comparison – our financial system is pretty sound.”

Brokers’ top priority

That most brokers in the industry want to achieve high compliance and do the best by their clients is probably fair to say.

“I think brokers have a very real concern that they are compliant with the law. I would say it’s probably on the top of mind with just about every broker that I speak to,” said Vow CEO Tim Brown, who explained that their compliance webinars were the best attended of all of Vow’s webinars.

One of Australia’s largest aggregation groups, Vow has a strong presence in compliance training for its brokers and runs a broker survey every six months. “Compliance is our most highly regarded area,” says Brown. “Our compliance area gets a 93% satisfaction rating, which shows they really value the education that we give them through our compliance.”

The aggregator also runs workshops that give brokers the opportunity to bring in their own files and discuss them. “People are able to have an open discussion without feeling threatened that they are going to get caught out. We find, educationally wise, they learn more from that experience than by us going and doing audits.”

While compulsory for those under Vow’s licence, brokers are finding the workshops so useful that those with their own licences are requesting that the aggregator runs similar workshops for a fee.

“They’ve been requesting that they want to attend our workshops, and they want us to do audits on them. It would give us some comfort, too, to know they are being compliant, albeit they’re not under our licence.”

Brown’s background in banking has placed him in a good position to compare the retail and broker channels.

“Most brokers have been in the industry a long time; they tend to have come out of major banks and so they tend to be well trained anyway and they know what not to do. They’ve got integrity and they know that their licence can be put at risk if they put a client into a loan that they can’t afford or that isn’t the right product for them.”

Broker-originated lending stands tall

MPA spoke to three lenders, who explained why the future was looking bright for the broker channel – and said third-party originated loans were ticking all the boxes.

Australia’s largest customer-owned bank, Heritage Bank, sources 50% of its mortgage loans through brokers and 50% from its retail network. The bank has also had an exceedingly strong year in loan origination through its broker partners, head of third party channels David Ure said. “This channel gives us access to markets across Australia,” he said. “Our relationship with the channel is considered very important.”

Ure said the bank’s main risk associated with loans introduced through a third party was in receiving/assessing and approving loan applications. “However, this risk is well mitigated through legislation and compliance requirements within the industry, as well as Heritage’s relationship with our broker partners,” he said.

But for ING Direct head of broker distribution Mark Woolnough, brokers don’t introduce any material risk into the process. “We’ve been working with brokers for a long time, nearing 20 years now, and we’ve always said to brokers and internally, they are essentially an extension of our own sales team. Being a branchless bank we don’t have a face-to-face or mobile sales network. We see our broker partners as the extension of our sales force, and therefore they’re effectively seen as our shopfront.”

He said brokers accounted for more than 20% of ING Direct’s lending business and there was no significant difference regarding approvals, defaults or refinances between direct and broker customers. “For us, there’s no statistical difference because our focus is not on just getting people into their homes but to make sure they stay in their homes longterm, which is reflected in where we pitch our products and our credit policy and our appetite to help customers.”

ME’s general manager brokers Lino Pelaccia said his bank’s experience of working with brokers had been “extremely positive”, with half of ME’s home loan sales originating from brokers in the past year.

“Brokers run professional, risk-averse businesses that are compliant and accredited with industry bodies,” said Pelaccia. “Brokers are also a great source for instant feedback on the state of the market and how our products and services are being received.”

ME plans to expand its broker network and expects it to generate 55% of home loan settlements over the next three years, totalling $3.3bn in FY16 and increasing to $5.3bn in FY18. “Brokers are a valued sales channel for ME, and the broker channel is critical to our growth plans going forward.”