MPA talks to the top three online platforms leading the way in the rapidly expanding small business lending sector

.jpg)

The entrepreneurial dream is strong in Australia – around one in three of us is keen to own a business, according to The Lure of Entrepreneurship report from NAB.

The survey showed about 40% of budding entrepreneurs and 75% of existing business owners need or needed less than $50,000 to get their business up and running, and almost half of existing business owners (46%) started out with less than $5,000.

The report also listed insufficient funds and generating enough income among the key inhibitors to starting a business, but with the rise of online lending platforms, it is now easier than ever for small businesses to get the extra capital they need to grow. Unsecured business lenders and their high speed, stress-free application processes are making a big difference for SMEs. MPA caught up with the three that are pioneering the way forward.

Up and up

“The size of the small business lending problem we solve is huge,” says Beau Bertoli, joint CEO of Australian-owned Prospa. “There are over 2 million small business owners in Australia, and at any point in time, roughly 20% of them are looking for funding to help manage cash flow or grow. We think small business lending will grow into a multi-billion-dollar market, potentially reaching $20 billion in five years.”

Lachlan Heussler, the Australia/New Zealand managing director for Spotcap, a platform also based in London and Amsterdam, says that although the sector is relatively new and has only been around in Australia for about six years, the scale of growth in the last 12 months is phenomenal.

“You’re talking large triple-digit growth for the industry as a whole,” he says. “Whereas a few years ago, we were talking about the tens of millions, right now we’re talking about the hundreds of millions, and my view is, within the next three to five years, we’ll be talking in the billions.”

Turnaround times can be within 24 hours now, Heussler says, if not sooner. “Before the rise of the online lending sector, it was a very, very time-consuming and difficult process for [business owners] to approach one of the Big Four or even some of the second-tier lenders to get a loan.”

Aris Allegos, co-founder and CEO of Moula, says part of the reason for this rapid growth is that people feel more comfortable sharing data from their accounting solutions, compared to just three years ago, when there was greater concern over privacy and data security.

“We’ve gotten to a point today where, quite literally, almost everyone permissions data to us,” Allegos says. “They’ve come to trust us as a brand, number one, and also they’ve come to understand that the data that sits within their accounting solution is effectively empowering them to get a loan. They’re effectively trading their data for a product, and that’s been a massive evolution over the course of probably the last 18 months, where we’ve seen it become quite pervasive. People just accept that this is the reality in 2017.”

Allegos points out that it is part of Moula’s role to create further awareness among businesses over the next five years to grow the sector. “We’re in a great position, all of us platforms, in that it’s a significant market that isn’t going away,” he says. “I don’t perceive that it’s a market that the traditional banks necessarily have the capacity to play in.”

“We’re in a great position, all of us platforms, in that it’s a significant market that isn’t going away – I don’t perceive that it’s a market that the traditional banks necessarily have the capacity to play in” Aris Allegos, Moula

“We’re in a great position, all of us platforms, in that it’s a significant market that isn’t going away – I don’t perceive that it’s a market that the traditional banks necessarily have the capacity to play in” Aris Allegos, Moula

Spotcap’s Heussler agrees. “For us – not only Spotcap, but my friendly competitors as well – the onus is on us to grow the industry as a whole, and the thing that’s holding us back is just a lack of awareness from both the broker community and the end users – the small businesses. We just like the brokers and their clients to think of us first because there’s no need to go to the banks anymore to try and get this type of financing.”

Matt Bauld, head of sales and business development at Prospa, says platforms like his provide a solution the big banks cannot. “Before we entered the market with our innovative technology and focus on customer experience,” he says, “the application process for small business owners needing finance was difficult and time-consuming. Now it’s fast and easy.”

More business from businesses

From the broker’s perspective, although these unsecured loans are short-term – up to 12 months in duration – and hence have no trail, all three lenders insist the repeat business from these types of clients is high.

“A working capital product, by its nature, is relatively short in terms of duration,” Heussler says; however he adds, small businesses, particularly in Australia, have a continual need for working capital. “So what we find is the vast majority of our customers are coming back for second, third, fourth and fifth loans as part of that relationship with us, and the brokers are being compensated as part of that as well.”

“So that, for the broker, equates to a trail,” adds Allegos. “That’s what we’re effectively saying to brokers. When they come back for that second, third and fourth loan, that goes to the broker who made the original introduction. Insofar as how many loans those guys will keep coming back for, we’re still working that out. But if I hazard a guess, it’s going to be probably not dissimilar to the average life of a mortgage in Australia, which is around four to five years. So there are almost similar revenue streams available to the people who get into this segment.”

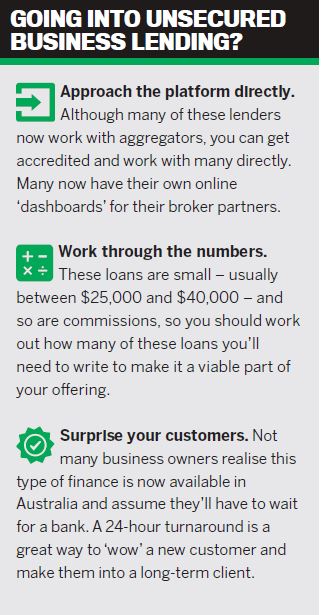

The average size of these unsecured business loans is usually between $25,000 and $40,000, but can range from $5,000 to $250,000. Applicants are often seeking working capital to buy stock or manage cash flow in their business, but may also want it for hiring staff, expanding operations or marketing campaigns, among other things. “There’s a whole range of reasons as to why they come and borrow from us,” Heussler says.

“What we find is the vast majority of our customers are coming back for second, third, fourth and fifth loans as part of that relationship with us, and the brokers are being compensated as part of that” Lachlan Heussler, Spotcap

“What we find is the vast majority of our customers are coming back for second, third, fourth and fifth loans as part of that relationship with us, and the brokers are being compensated as part of that” Lachlan Heussler, Spotcap

Brokers on the mind

Looking ahead, these three leading online lenders have their attention firmly set on the broker channel. “The broker channel, for us, is obviously critical – as they should be for any lending product in this country,” Allegos says, adding that around 50% to 60% of Moula’s business comes via brokers.

“We like the broker channel because they pre-qualify a lot of our loans,” he says; he claims Moula’s conversion rates through brokers are two times better than what they are through the direct channel. “Notwithstanding we’ve built a robust tech platform that can do a lot of the analytics, it still helps to pre-qual who comes through the machine,” he says.

Along with brokers, accountants and financial planners are a very large part of Spotcap’s distribution plans, says Heussler, and the company is working with most of Australia’s large aggregators to reach brokers via their distribution networks.

Prospa’s Bertoli agrees that brokers are a vital part of his company’s long-term strategy. “We’ve been working with brokers for nearly four years now,” he says, “and they will continue to be an integral part of our business moving forward.”

The survey showed about 40% of budding entrepreneurs and 75% of existing business owners need or needed less than $50,000 to get their business up and running, and almost half of existing business owners (46%) started out with less than $5,000.

The report also listed insufficient funds and generating enough income among the key inhibitors to starting a business, but with the rise of online lending platforms, it is now easier than ever for small businesses to get the extra capital they need to grow. Unsecured business lenders and their high speed, stress-free application processes are making a big difference for SMEs. MPA caught up with the three that are pioneering the way forward.

Up and up

“The size of the small business lending problem we solve is huge,” says Beau Bertoli, joint CEO of Australian-owned Prospa. “There are over 2 million small business owners in Australia, and at any point in time, roughly 20% of them are looking for funding to help manage cash flow or grow. We think small business lending will grow into a multi-billion-dollar market, potentially reaching $20 billion in five years.”

Lachlan Heussler, the Australia/New Zealand managing director for Spotcap, a platform also based in London and Amsterdam, says that although the sector is relatively new and has only been around in Australia for about six years, the scale of growth in the last 12 months is phenomenal.

“You’re talking large triple-digit growth for the industry as a whole,” he says. “Whereas a few years ago, we were talking about the tens of millions, right now we’re talking about the hundreds of millions, and my view is, within the next three to five years, we’ll be talking in the billions.”

Turnaround times can be within 24 hours now, Heussler says, if not sooner. “Before the rise of the online lending sector, it was a very, very time-consuming and difficult process for [business owners] to approach one of the Big Four or even some of the second-tier lenders to get a loan.”

Aris Allegos, co-founder and CEO of Moula, says part of the reason for this rapid growth is that people feel more comfortable sharing data from their accounting solutions, compared to just three years ago, when there was greater concern over privacy and data security.

“We’ve gotten to a point today where, quite literally, almost everyone permissions data to us,” Allegos says. “They’ve come to trust us as a brand, number one, and also they’ve come to understand that the data that sits within their accounting solution is effectively empowering them to get a loan. They’re effectively trading their data for a product, and that’s been a massive evolution over the course of probably the last 18 months, where we’ve seen it become quite pervasive. People just accept that this is the reality in 2017.”

Allegos points out that it is part of Moula’s role to create further awareness among businesses over the next five years to grow the sector. “We’re in a great position, all of us platforms, in that it’s a significant market that isn’t going away,” he says. “I don’t perceive that it’s a market that the traditional banks necessarily have the capacity to play in.”

“We’re in a great position, all of us platforms, in that it’s a significant market that isn’t going away – I don’t perceive that it’s a market that the traditional banks necessarily have the capacity to play in” Aris Allegos, MoulaSpotcap’s Heussler agrees. “For us – not only Spotcap, but my friendly competitors as well – the onus is on us to grow the industry as a whole, and the thing that’s holding us back is just a lack of awareness from both the broker community and the end users – the small businesses. We just like the brokers and their clients to think of us first because there’s no need to go to the banks anymore to try and get this type of financing.”

Matt Bauld, head of sales and business development at Prospa, says platforms like his provide a solution the big banks cannot. “Before we entered the market with our innovative technology and focus on customer experience,” he says, “the application process for small business owners needing finance was difficult and time-consuming. Now it’s fast and easy.”

More business from businesses

From the broker’s perspective, although these unsecured loans are short-term – up to 12 months in duration – and hence have no trail, all three lenders insist the repeat business from these types of clients is high.

“A working capital product, by its nature, is relatively short in terms of duration,” Heussler says; however he adds, small businesses, particularly in Australia, have a continual need for working capital. “So what we find is the vast majority of our customers are coming back for second, third, fourth and fifth loans as part of that relationship with us, and the brokers are being compensated as part of that as well.”

“So that, for the broker, equates to a trail,” adds Allegos. “That’s what we’re effectively saying to brokers. When they come back for that second, third and fourth loan, that goes to the broker who made the original introduction. Insofar as how many loans those guys will keep coming back for, we’re still working that out. But if I hazard a guess, it’s going to be probably not dissimilar to the average life of a mortgage in Australia, which is around four to five years. So there are almost similar revenue streams available to the people who get into this segment.”

The average size of these unsecured business loans is usually between $25,000 and $40,000, but can range from $5,000 to $250,000. Applicants are often seeking working capital to buy stock or manage cash flow in their business, but may also want it for hiring staff, expanding operations or marketing campaigns, among other things. “There’s a whole range of reasons as to why they come and borrow from us,” Heussler says.

“What we find is the vast majority of our customers are coming back for second, third, fourth and fifth loans as part of that relationship with us, and the brokers are being compensated as part of that” Lachlan Heussler, SpotcapBrokers on the mind

Looking ahead, these three leading online lenders have their attention firmly set on the broker channel. “The broker channel, for us, is obviously critical – as they should be for any lending product in this country,” Allegos says, adding that around 50% to 60% of Moula’s business comes via brokers.

“We like the broker channel because they pre-qualify a lot of our loans,” he says; he claims Moula’s conversion rates through brokers are two times better than what they are through the direct channel. “Notwithstanding we’ve built a robust tech platform that can do a lot of the analytics, it still helps to pre-qual who comes through the machine,” he says.

Along with brokers, accountants and financial planners are a very large part of Spotcap’s distribution plans, says Heussler, and the company is working with most of Australia’s large aggregators to reach brokers via their distribution networks.

Prospa’s Bertoli agrees that brokers are a vital part of his company’s long-term strategy. “We’ve been working with brokers for nearly four years now,” he says, “and they will continue to be an integral part of our business moving forward.”