Brokers already account for the majority of asset and equipment finance business in the SME market, so diversification success or failure depends on finding your focus

Asset and equipment finance is something today’s mortgage brokers hear a lot about. As lenders seek to expand distribution by introducing new products and aggregators diversify out of pure mortgages, the barrage of encouragement to diversify can be deafening. But is it right for everyone?

Prolease and Finance has been in the asset finance market since 1989. Owner Darren Goodman says the company handles primarily car finance due to high demand in the small business market, but will finance everything from trucks and forklifts to printers and copiers.

Goodman, who is also responsible for Vow Financial’s referral business, says the decision to expand into asset finance depends on the broker and the business, and whether they have the right infrastructure in place and skill set to succeed in the market they choose.

In the end, it seems success in asset and equipment finance may depend on your focus.

Financing cars

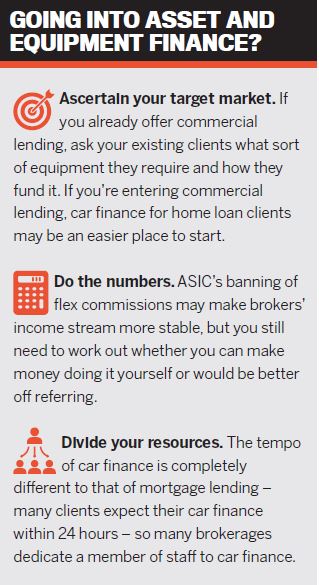

ANZ’s general manager of commercial origination, Cosi De Angelis, says car finance can be a good place for brokers moving into the asset finance market to start. At present, he says, 40% of the equipment finance market is cars, making it a big potential market for brokers.

“For the mortgage broker, that is the easiest asset class to start targeting,” he says. “Cars, trucks and equipment may seem a little difficult, but for the average broker, car finance is really easy.”

There’s also a high degree of crossover between a broker’s core mortgage business and the need for a car. “We believe that within 12 months of a client changing the mortgage on their home or buying a new house, they’re looking at buying a car,” De Angelis says. “There seems to a high correlation between that event and the purchase of a new vehicle.”

If brokers don’t offer car finance, they may eventually be forced to. Motor dealers themselves don’t seem to be hesitating in their own moves to sell mortgage brokers’ bread and butter.

“Car dealers are out there today, doing exactly what mortgage brokers are looking to do, but in reverse,” De Angelis says. “Car dealers are looking to obtain credit licenses and sell products other than the car to their customer base. If brokers aren’t able to ringfence their customers, then they may find themselves losing the mortgage.”

However, Goodman says that while getting into the car market might seem an easy segue, it can actually be a daunting prospect at first. “There’s no easy way to just jump into it,” he says.

That’s partly because brokers need the right infrastructure to be able to compete. “Some brokers find the car market way too competitive and aggressive, and some avoid it completely,” he says. “With cars, you have to be quick – people find a car today, and they want to pick it up this weekend – so you need the systems and processes in place to do that.”

Lenders are also reluctant to accredit new car finance brokers. “If you’re not giving lenders volume, often they won’t accredit you,” Goodman says. “The only way to get that is either through a mortgage aggregator that has a relationship with them, or by linking up with an existing broker and running it through their business as an authorized representative.”

Because each lender also has different software for car finance deals, brokers really need experience to be effective. The sum of these factors is a chicken-and-egg scenario where brokers need experience to do deals, but are unable to get easy experience upfront.

Then there’s the big question: Is the commission worth it?

“What we find is a lot of the mortgage brokers who think, ‘Let’s get into this’ and start doing it themselves have found the amount of work versus income doesn’t seem to warrant it,” Goodman says. “A lot prefer to align with someone and refer to them and get a referral commission, so they are not doing all the work but are offering the service to their customers.

“We’ve got a lot of experience dealing with mortgage brokers,” he continues. “The key message I often give is they are far better off focusing on a $1 million mortgage deal than a $20,000 car deal. They are different beasts in terms of pace and time, and if they don’t have the infrastructure, they can end up offering a poorer service to their clients, which they don’t want to do.”

Credit and commission

Prolease built its own referral base primarily through relationships with accountants, in addition to wholesale car dealers. That was in line with a strategy to get close to a more reliable white-collar market with good businesses that require regular funding.

While Goodman is a generalist, he argues a good way to enter the market today is to pick a niche. “Find an industry you have connections and links in,” he says, “and focus on equipment in that industry as opposed to trying to beat all the rest of the guys in the car market.”

Goodman says business as a whole looks good this year when measured by enquiries and growth. However, there are other factors coming into play that are requiring asset finance brokers like Prolease to become better jugglers of clients and credit.

“The risk of a Royal Commission into banking means a lot of lenders have tightened up on credit policy and are changing their policies slightly, like they did during the GFC,” he says. “Whereas before if you had 10 enquiries and you may do eight or so because you lose two of them to competitors, now you are only doing six because you can’t get two across the line.”

Non-conforming lenders are stepping into the gap. Although clients need to pay a premium, they are often more than willing if they don’t fit the shrinking appetite of the major banks.

“Often mainstream lenders are concerned about the type of equipment they are financing, whereas non-conforming lenders are concerned more about the strength of the applicant,” Goodman says. “Whereas a major lender doesn’t want the asset on their books, the non-conforming lender sees someone who looks as if they are going to pay.”

Alleasing is one player with a new broker model, which launched at the end of 2016. David Onto, who heads up intermediary distribution, says the business has got off to a good start with $134 million in deals, thanks to its unearthing of some quality brokers.

Alleasing allows customers who can’t access any more senior capital from their banks to realise the value of existing assets through arrangements like sale and leaseback. “Where banks are interested in brand-new assets with known residual value at any given time,” Onto says, “our expertise is managing the value of an asset at any given stage of its life cycle.”

Onto says brokers with access to providers like Alleasing – ones who know where to go for their clients – are ahead, because they are less about the product and more about the solution. “If you offer what everyone else is in the marketplace, it’s difficult to derive real value for that,” he says, “but if you have a niche, you put yourself in a better position.”

This plays into the commission equation. Because commissions are by negotiation in the asset and equipment finance market, brokers doing a $100,000 piece of equipment may end up earning minimal commission on the deal if they face lender competition. With interest rates so low, brokers are also struggling to justify a good rate of commission for their services.

Onto says this is when providing solutions counts. “If you can add a bigger fix than would have existed otherwise, you can create more elasticity in the brokerage itself,” he says. “There’s an amazing opportunity for brokers. The average business banker stays in their role these days no more than 18 months. Brokers can offer truly consistent service and relationships that the banks don’t anymore, and that is really their competitive advantage.”

Mix and match

AFG’s commercial general manager, Keiran Evans, has seen an increase in the number of new lenders entering the asset finance space, leading to increased market competition. “It is also bringing improvement in technology as the new entrants attempt to take advantage of the lack of platform investment by many of the existing dominant lenders,” he says.

Evans thinks brokers have a significant opportunity in the market. “There is no doubt customers are seeking a more holistic service proposition to their finance needs, and brokers have a rare opportunity to satisfy this demand,” he says. “Expanding brokers’ core competencies beyond a single finance channel – be that asset, commercial or residential – will ultimately deepen the broker/customer relationship and likely lead to other opportunities.

Note: Just as this article went to print, ASIC declared they were banning the use of flex commissions for brokers and car dealers in the car finance market. Brokers will be able to offer discounted interest rates and thus earn lower commission.

Prolease and Finance has been in the asset finance market since 1989. Owner Darren Goodman says the company handles primarily car finance due to high demand in the small business market, but will finance everything from trucks and forklifts to printers and copiers.

Goodman, who is also responsible for Vow Financial’s referral business, says the decision to expand into asset finance depends on the broker and the business, and whether they have the right infrastructure in place and skill set to succeed in the market they choose.

In the end, it seems success in asset and equipment finance may depend on your focus.

Financing cars

ANZ’s general manager of commercial origination, Cosi De Angelis, says car finance can be a good place for brokers moving into the asset finance market to start. At present, he says, 40% of the equipment finance market is cars, making it a big potential market for brokers.

“For the mortgage broker, that is the easiest asset class to start targeting,” he says. “Cars, trucks and equipment may seem a little difficult, but for the average broker, car finance is really easy.”

There’s also a high degree of crossover between a broker’s core mortgage business and the need for a car. “We believe that within 12 months of a client changing the mortgage on their home or buying a new house, they’re looking at buying a car,” De Angelis says. “There seems to a high correlation between that event and the purchase of a new vehicle.”

If brokers don’t offer car finance, they may eventually be forced to. Motor dealers themselves don’t seem to be hesitating in their own moves to sell mortgage brokers’ bread and butter.

“Car dealers are out there today, doing exactly what mortgage brokers are looking to do, but in reverse,” De Angelis says. “Car dealers are looking to obtain credit licenses and sell products other than the car to their customer base. If brokers aren’t able to ringfence their customers, then they may find themselves losing the mortgage.”

However, Goodman says that while getting into the car market might seem an easy segue, it can actually be a daunting prospect at first. “There’s no easy way to just jump into it,” he says.

That’s partly because brokers need the right infrastructure to be able to compete. “Some brokers find the car market way too competitive and aggressive, and some avoid it completely,” he says. “With cars, you have to be quick – people find a car today, and they want to pick it up this weekend – so you need the systems and processes in place to do that.”

Lenders are also reluctant to accredit new car finance brokers. “If you’re not giving lenders volume, often they won’t accredit you,” Goodman says. “The only way to get that is either through a mortgage aggregator that has a relationship with them, or by linking up with an existing broker and running it through their business as an authorized representative.”

Because each lender also has different software for car finance deals, brokers really need experience to be effective. The sum of these factors is a chicken-and-egg scenario where brokers need experience to do deals, but are unable to get easy experience upfront.

Then there’s the big question: Is the commission worth it?

“What we find is a lot of the mortgage brokers who think, ‘Let’s get into this’ and start doing it themselves have found the amount of work versus income doesn’t seem to warrant it,” Goodman says. “A lot prefer to align with someone and refer to them and get a referral commission, so they are not doing all the work but are offering the service to their customers.

“We’ve got a lot of experience dealing with mortgage brokers,” he continues. “The key message I often give is they are far better off focusing on a $1 million mortgage deal than a $20,000 car deal. They are different beasts in terms of pace and time, and if they don’t have the infrastructure, they can end up offering a poorer service to their clients, which they don’t want to do.”

TAKING ON THE BANKS

Brokers are far from outliers in the asset finance market. With a annual market volume of $40 billion and receivables worth $100 billion, brokers already have an overall 61.6% market share, according to the Commercial Asset Finance Brokers Association of Australia.

President David Gandolfo says the interesting fact is that brokers are not only dominating the micro and SME spaces, but are also penetrating the corporate and institutional markets – typically the domain of the mainstream lenders rather than asset finance brokers.

However, it’s not an easy road. Gandolfo says brokers entering the market should realize it is complex and relational, which makes it different from writing mortgage business.

“Asset finance isn’t as simple as it looks,” he says. “You need some degree of experience and commercial knowledge in order to package loans appropriately in terms of their tax effectiveness. Asset finance brokers are also very relational, not transactional. Typically, you have commercial clients with ongoing requirements for upgrading and replacing machinery, equipment, and the means by which they generate income.”

Gandolfo recommends brokers get educated before they dive into the market. “Our brokers are typically asset finance professionals,” he says. “Some mortgage brokers come from sales backgrounds, but our members all come from finance backgrounds.”

Brokers are far from outliers in the asset finance market. With a annual market volume of $40 billion and receivables worth $100 billion, brokers already have an overall 61.6% market share, according to the Commercial Asset Finance Brokers Association of Australia.

President David Gandolfo says the interesting fact is that brokers are not only dominating the micro and SME spaces, but are also penetrating the corporate and institutional markets – typically the domain of the mainstream lenders rather than asset finance brokers.

However, it’s not an easy road. Gandolfo says brokers entering the market should realize it is complex and relational, which makes it different from writing mortgage business.

“Asset finance isn’t as simple as it looks,” he says. “You need some degree of experience and commercial knowledge in order to package loans appropriately in terms of their tax effectiveness. Asset finance brokers are also very relational, not transactional. Typically, you have commercial clients with ongoing requirements for upgrading and replacing machinery, equipment, and the means by which they generate income.”

Gandolfo recommends brokers get educated before they dive into the market. “Our brokers are typically asset finance professionals,” he says. “Some mortgage brokers come from sales backgrounds, but our members all come from finance backgrounds.”

BEATING THE BARBARIANS

Stratton, one of the largest asset finance brokers in Australia, has noticed over the last 12 months that relationships with customers are becoming more strategic rather than transactional. Business customers are no longer just interested in rates.

“They’re focusing on a range of other value drivers, from responsiveness to more sustainable solutions and partners that can play a strategic part in the growth of their business,” says John Alvarez, Stratton’s head of commercial and third party.

Stratton is investing in infrastructure and capabilities that will allow it to capture more relevant customer information, to enable it to better understand customer needs and work with lenders to create better solutions. “The old model, where broker behaviour is modelled on reacting to customer needs when they become a problem, is dying,” Alvarez says. “The new model is one where brokers nurture relationships, pre-empt customer needs and proactively seek ways to create value.”

Stratton also expects fintechs to play a greater role. “Like barbarians at the gates of Rome, they are looking to disrupt the incumbents,” Alvarez says. “We love it, and continue to challenge ourselves to deliver differentiated products and a seamless customer experience.”

Stratton, one of the largest asset finance brokers in Australia, has noticed over the last 12 months that relationships with customers are becoming more strategic rather than transactional. Business customers are no longer just interested in rates.

“They’re focusing on a range of other value drivers, from responsiveness to more sustainable solutions and partners that can play a strategic part in the growth of their business,” says John Alvarez, Stratton’s head of commercial and third party.

Stratton is investing in infrastructure and capabilities that will allow it to capture more relevant customer information, to enable it to better understand customer needs and work with lenders to create better solutions. “The old model, where broker behaviour is modelled on reacting to customer needs when they become a problem, is dying,” Alvarez says. “The new model is one where brokers nurture relationships, pre-empt customer needs and proactively seek ways to create value.”

Stratton also expects fintechs to play a greater role. “Like barbarians at the gates of Rome, they are looking to disrupt the incumbents,” Alvarez says. “We love it, and continue to challenge ourselves to deliver differentiated products and a seamless customer experience.”

Credit and commission

Prolease built its own referral base primarily through relationships with accountants, in addition to wholesale car dealers. That was in line with a strategy to get close to a more reliable white-collar market with good businesses that require regular funding.

While Goodman is a generalist, he argues a good way to enter the market today is to pick a niche. “Find an industry you have connections and links in,” he says, “and focus on equipment in that industry as opposed to trying to beat all the rest of the guys in the car market.”

Goodman says business as a whole looks good this year when measured by enquiries and growth. However, there are other factors coming into play that are requiring asset finance brokers like Prolease to become better jugglers of clients and credit.

“The risk of a Royal Commission into banking means a lot of lenders have tightened up on credit policy and are changing their policies slightly, like they did during the GFC,” he says. “Whereas before if you had 10 enquiries and you may do eight or so because you lose two of them to competitors, now you are only doing six because you can’t get two across the line.”

Non-conforming lenders are stepping into the gap. Although clients need to pay a premium, they are often more than willing if they don’t fit the shrinking appetite of the major banks.

“Often mainstream lenders are concerned about the type of equipment they are financing, whereas non-conforming lenders are concerned more about the strength of the applicant,” Goodman says. “Whereas a major lender doesn’t want the asset on their books, the non-conforming lender sees someone who looks as if they are going to pay.”

Alleasing is one player with a new broker model, which launched at the end of 2016. David Onto, who heads up intermediary distribution, says the business has got off to a good start with $134 million in deals, thanks to its unearthing of some quality brokers.

Alleasing allows customers who can’t access any more senior capital from their banks to realise the value of existing assets through arrangements like sale and leaseback. “Where banks are interested in brand-new assets with known residual value at any given time,” Onto says, “our expertise is managing the value of an asset at any given stage of its life cycle.”

Onto says brokers with access to providers like Alleasing – ones who know where to go for their clients – are ahead, because they are less about the product and more about the solution. “If you offer what everyone else is in the marketplace, it’s difficult to derive real value for that,” he says, “but if you have a niche, you put yourself in a better position.”

This plays into the commission equation. Because commissions are by negotiation in the asset and equipment finance market, brokers doing a $100,000 piece of equipment may end up earning minimal commission on the deal if they face lender competition. With interest rates so low, brokers are also struggling to justify a good rate of commission for their services.

Onto says this is when providing solutions counts. “If you can add a bigger fix than would have existed otherwise, you can create more elasticity in the brokerage itself,” he says. “There’s an amazing opportunity for brokers. The average business banker stays in their role these days no more than 18 months. Brokers can offer truly consistent service and relationships that the banks don’t anymore, and that is really their competitive advantage.”

Mix and match

AFG’s commercial general manager, Keiran Evans, has seen an increase in the number of new lenders entering the asset finance space, leading to increased market competition. “It is also bringing improvement in technology as the new entrants attempt to take advantage of the lack of platform investment by many of the existing dominant lenders,” he says.

Evans thinks brokers have a significant opportunity in the market. “There is no doubt customers are seeking a more holistic service proposition to their finance needs, and brokers have a rare opportunity to satisfy this demand,” he says. “Expanding brokers’ core competencies beyond a single finance channel – be that asset, commercial or residential – will ultimately deepen the broker/customer relationship and likely lead to other opportunities.

Note: Just as this article went to print, ASIC declared they were banning the use of flex commissions for brokers and car dealers in the car finance market. Brokers will be able to offer discounted interest rates and thus earn lower commission.