Bankwest’s new general manager of broker sales tells MPA why a better bank experience for customers means more business for the non-major’s broker partners

Bankwest’s new general manager of broker sales tells MPA why a better bank experience for customers means more business for the non-major’s broker partners.

MPA: How will Bankwest differentiate itself in a crowded non-major market?

Stewart Saunders: We’re a broker-focused organisation, with the majority of our mortgage business coming from brokers. We were one of the fi rst banks to work with brokers, more than 20 years ago, and those relationships are still incredibly valuable to us.

Bankwest is in a relatively unique position, as we operate in two distinct markets. Here in WA, our home state, we operate as a major player with signifi cant market share that’s been built over a long period of time, which means our focus is on maintaining those relationships with brokers who use us consistently as a primary bank. Whereas on the east coast, and SA/NT, we operate as a non-major alternative, meaning we need to have a compelling offer for a broker to not only give us a go, but use us more consistently.

In order to be consistent in a crowded lender market it’s important to be consistent across all aspects of our offering, so not just rates, but credit policy, turnaround times, BDM support, relationships with brokers, commissions and overall support of brokers. We need to be able to deliver consistently on expectations, with the aim to actually out-deliver on what brokers expect from their bank.

We’ve also got an outstanding model for our broker support, where all our BDMs have a dedicated broker support officer, which ensures we can respond to all broker enquiries in a very timely manner. With that in mind, I believe we have one of the best models for supporting brokers, who consistently provide great feedback on our team’s performance and support.

MPA: What does Bankwest’s target customer look like?

SS: Bankwest has been known traditionally as a very strong lender in the fi rst home buyer segment, due to our competitive offering over time in the higher LVR space. Whilst this has, and continues to be, a strong part of our offering, we are looking to grow in other areas of the market. So, recently, we’ve focused a signifi cant effort on driving a competitive offering for homeowners, particularly those who’ve built up some equity and may be looking to purchase an investment property, refi nance their home, upgrade to a larger home, or potentially downsize their property.

MPA: So you’re not deterred by the recent regulator action around investor lending?

SS: Bankwest has been proactive in ensuring that we’re able to meet the guidance put forward by APRA regarding investment lending. In order to manage this, we’ve had to make a number of changes to our products, policy and pricing over the past year. Subsequently, we’ve been able to manage our investor lending portfolio within these parameters from APRA, and have created some capacity to further grow our investor book.

We’ve made some positive changes to return to a sustainable growth trajectory in this segment, an example of which being our increased maximum LVR to 90% for investment lending. This was 80% previously, which was implemented in part following APRA’s guidance to banks. Having a look forward, the APRA guidance remains in place moving into 2016, which limits banks’ investor lending growth to no more than 10% year-on-year. This will limit supply to some degree, but as banks manage to lower their growth rates to that required by the regulator, banks’ individual appetites will increase and I’d expect to see some greater competition in investor lending in the year ahead.

We’ve made some positive changes to return to a sustainable growth trajectory in this segment, an example of which being our increased maximum LVR to 90% for investment lending. This was 80% previously, which was implemented in part following APRA’s guidance to banks. Having a look forward, the APRA guidance remains in place moving into 2016, which limits banks’ investor lending growth to no more than 10% year-on-year. This will limit supply to some degree, but as banks manage to lower their growth rates to that required by the regulator, banks’ individual appetites will increase and I’d expect to see some greater competition in investor lending in the year ahead.

MPA: Most brokers are aware of the relationship between Bankwest and Commonwealth Bank. How does this help Bankwest?

SS: Bankwest is a division of CBA and operates under one banking license. Effectively, however, we run a separate business. That includes our customer-facing units, such as our distribution businesses. Bankwest determines its own pricing, product offerings, markets and risk appetite, which does include our credit policy.

We target customers who are looking for an alternative to the major banks, who are looking to bank with a smaller organisation offering personalised service. I do receive feedback from brokers on the difference on offering between CBA and Bankwest and vice versa, which isn’t a bad thing. We’re able to target different customers to ensure we can SS: Bankwest has a very strong focus on brokers as the majority of mortgages are originated through brokers. We have beensuccessful in building a strong offering in the market, however future growth will be dependent on further investment in the channel.

We’ve recently embarked on a significant project, which will underpin our offering in the future. It’s focused on delivering a market-leading customer experience.

While customer experience is important for all banks, it’s particularly important to the broker channel. Talking to brokers, it’s apparent that a significant proportion of their new business comes from referrals of their existing clients, or repeat business, and having a bank that can deliver in excess of customer expectations will help a broker build their business. That’s why Bankwest is making a significant strategic investment in our overall home loan customer experience… We’re looking at all aspects of the home loan process, from consideration right on to the on-boarding and post-fulfilment of those loans.

MPA: When we’re talking about customer experience, is this a matter of turnaround time, or of someone being available on the phone, or simplified paperwork? What’s the key improvement Bankwest is looking to make?

SS: It’s absolutely all of those points Early on in the project we actively engaged with brokers through our design workshops, to ensure that their needs were integral to the planning throughout this project. We’re investing in better leveraging existing thirdparty data – process simplification and digitisation of key tasks that are currently causing delays and rework.

Crucially, while this project is going – which will probably take around 18 months – we’re not sitting still. We are looking at further tactical initiatives to bring improvements across our offering and processes, so dealing with Bankwest is easier for brokers.

We’ve already seen the delivery to market of a number of initiatives, including a new upfront valuation portal for brokers, which was delivered in the second half of last year and has been really well received by brokers. In addition to this we’ve had further refinements in back office processing, which has seen us consistently deliver on our service levels for decisions, even in periods where we’ve had significant volumes of home loans.

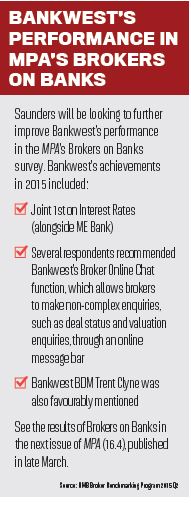

We’ve also put in place a new broker survey to welcome direct feedback from brokers about the support our BDMs are providing. That’s really important as we look for ways to improve our customer experience, based on feedback from brokers.

MPA: Recently, other non-majors have experienced problems when enormously successful offers resulted in applications – and turnaround times - going through the roof. How will Bankwest stop this happening?

SS: I think every bank has a capacity of what they’re able to service, so dependent on the quantity of applications that come through, all organisations could potentially struggle. What we’re working to ensure is that we can consistently deliver based on our forecasts for what our volumes are. We have seen some recent significant volumes of applications, which we’ve been able to deal with within our service levels, which has been a great achievement for our processing areas, and has shown some really good improvement in how we’re able to handle applications better, and process applications as they come through.

MPA: In the longer term – the next 24 months – how would you like Bankwest to be perceived by brokers ?

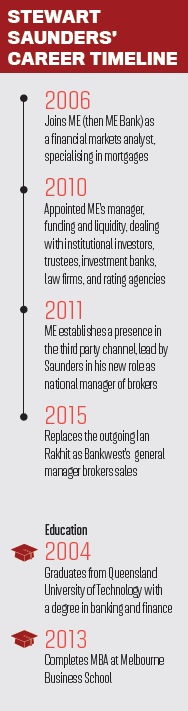

SS: It’s been just over six months now since I joined Bankwest, and it’s been a terrific challenge so far. I’ve certainly had a focus for us to have a clear plan and strategy in order to be able to continue to build on the success the business has had today. We’ve had a clear vision for Bankwest – we want to be the best by delivering on what matters for our customers. In order to achieve this vision, our strategy is underpinned by four key pillars, which includes customer experience, the core pillar, underpinned by our people and culture, simplicity approach and driving sustainable growth.

From a broker’s point of view, we’ve developed a detailed three-year roadmap with short-, medium- and long-term horizons, where we’ll look to start to realise benefits while delivering larger, more complicated initiatives. We know brokers provide the majority of business at Bankwest and they are absolutely a key partner in achieving that vision. The broker channel remains a core focus for Bankwest and we look forward to continuing to support brokers in their businesses. I think the direction we’re moving in is really exciting and I have no doubts that 2016 will be a really big year for Bankwest.

MPA: How will Bankwest differentiate itself in a crowded non-major market?

Stewart Saunders: We’re a broker-focused organisation, with the majority of our mortgage business coming from brokers. We were one of the fi rst banks to work with brokers, more than 20 years ago, and those relationships are still incredibly valuable to us.

Bankwest is in a relatively unique position, as we operate in two distinct markets. Here in WA, our home state, we operate as a major player with signifi cant market share that’s been built over a long period of time, which means our focus is on maintaining those relationships with brokers who use us consistently as a primary bank. Whereas on the east coast, and SA/NT, we operate as a non-major alternative, meaning we need to have a compelling offer for a broker to not only give us a go, but use us more consistently.

In order to be consistent in a crowded lender market it’s important to be consistent across all aspects of our offering, so not just rates, but credit policy, turnaround times, BDM support, relationships with brokers, commissions and overall support of brokers. We need to be able to deliver consistently on expectations, with the aim to actually out-deliver on what brokers expect from their bank.

We’ve also got an outstanding model for our broker support, where all our BDMs have a dedicated broker support officer, which ensures we can respond to all broker enquiries in a very timely manner. With that in mind, I believe we have one of the best models for supporting brokers, who consistently provide great feedback on our team’s performance and support.

MPA: What does Bankwest’s target customer look like?

SS: Bankwest has been known traditionally as a very strong lender in the fi rst home buyer segment, due to our competitive offering over time in the higher LVR space. Whilst this has, and continues to be, a strong part of our offering, we are looking to grow in other areas of the market. So, recently, we’ve focused a signifi cant effort on driving a competitive offering for homeowners, particularly those who’ve built up some equity and may be looking to purchase an investment property, refi nance their home, upgrade to a larger home, or potentially downsize their property.

MPA: So you’re not deterred by the recent regulator action around investor lending?

SS: Bankwest has been proactive in ensuring that we’re able to meet the guidance put forward by APRA regarding investment lending. In order to manage this, we’ve had to make a number of changes to our products, policy and pricing over the past year. Subsequently, we’ve been able to manage our investor lending portfolio within these parameters from APRA, and have created some capacity to further grow our investor book.

We’ve made some positive changes to return to a sustainable growth trajectory in this segment, an example of which being our increased maximum LVR to 90% for investment lending. This was 80% previously, which was implemented in part following APRA’s guidance to banks. Having a look forward, the APRA guidance remains in place moving into 2016, which limits banks’ investor lending growth to no more than 10% year-on-year. This will limit supply to some degree, but as banks manage to lower their growth rates to that required by the regulator, banks’ individual appetites will increase and I’d expect to see some greater competition in investor lending in the year ahead.MPA: Most brokers are aware of the relationship between Bankwest and Commonwealth Bank. How does this help Bankwest?

SS: Bankwest is a division of CBA and operates under one banking license. Effectively, however, we run a separate business. That includes our customer-facing units, such as our distribution businesses. Bankwest determines its own pricing, product offerings, markets and risk appetite, which does include our credit policy.

We target customers who are looking for an alternative to the major banks, who are looking to bank with a smaller organisation offering personalised service. I do receive feedback from brokers on the difference on offering between CBA and Bankwest and vice versa, which isn’t a bad thing. We’re able to target different customers to ensure we can SS: Bankwest has a very strong focus on brokers as the majority of mortgages are originated through brokers. We have beensuccessful in building a strong offering in the market, however future growth will be dependent on further investment in the channel.

We’ve recently embarked on a significant project, which will underpin our offering in the future. It’s focused on delivering a market-leading customer experience.

While customer experience is important for all banks, it’s particularly important to the broker channel. Talking to brokers, it’s apparent that a significant proportion of their new business comes from referrals of their existing clients, or repeat business, and having a bank that can deliver in excess of customer expectations will help a broker build their business. That’s why Bankwest is making a significant strategic investment in our overall home loan customer experience… We’re looking at all aspects of the home loan process, from consideration right on to the on-boarding and post-fulfilment of those loans.

MPA: When we’re talking about customer experience, is this a matter of turnaround time, or of someone being available on the phone, or simplified paperwork? What’s the key improvement Bankwest is looking to make?

SS: It’s absolutely all of those points Early on in the project we actively engaged with brokers through our design workshops, to ensure that their needs were integral to the planning throughout this project. We’re investing in better leveraging existing thirdparty data – process simplification and digitisation of key tasks that are currently causing delays and rework.

Crucially, while this project is going – which will probably take around 18 months – we’re not sitting still. We are looking at further tactical initiatives to bring improvements across our offering and processes, so dealing with Bankwest is easier for brokers.

We’ve already seen the delivery to market of a number of initiatives, including a new upfront valuation portal for brokers, which was delivered in the second half of last year and has been really well received by brokers. In addition to this we’ve had further refinements in back office processing, which has seen us consistently deliver on our service levels for decisions, even in periods where we’ve had significant volumes of home loans.

We’ve also put in place a new broker survey to welcome direct feedback from brokers about the support our BDMs are providing. That’s really important as we look for ways to improve our customer experience, based on feedback from brokers.

MPA: Recently, other non-majors have experienced problems when enormously successful offers resulted in applications – and turnaround times - going through the roof. How will Bankwest stop this happening?

SS: I think every bank has a capacity of what they’re able to service, so dependent on the quantity of applications that come through, all organisations could potentially struggle. What we’re working to ensure is that we can consistently deliver based on our forecasts for what our volumes are. We have seen some recent significant volumes of applications, which we’ve been able to deal with within our service levels, which has been a great achievement for our processing areas, and has shown some really good improvement in how we’re able to handle applications better, and process applications as they come through.

MPA: In the longer term – the next 24 months – how would you like Bankwest to be perceived by brokers ?

SS: It’s been just over six months now since I joined Bankwest, and it’s been a terrific challenge so far. I’ve certainly had a focus for us to have a clear plan and strategy in order to be able to continue to build on the success the business has had today. We’ve had a clear vision for Bankwest – we want to be the best by delivering on what matters for our customers. In order to achieve this vision, our strategy is underpinned by four key pillars, which includes customer experience, the core pillar, underpinned by our people and culture, simplicity approach and driving sustainable growth.

From a broker’s point of view, we’ve developed a detailed three-year roadmap with short-, medium- and long-term horizons, where we’ll look to start to realise benefits while delivering larger, more complicated initiatives. We know brokers provide the majority of business at Bankwest and they are absolutely a key partner in achieving that vision. The broker channel remains a core focus for Bankwest and we look forward to continuing to support brokers in their businesses. I think the direction we’re moving in is really exciting and I have no doubts that 2016 will be a really big year for Bankwest.